Walmart’s Nasdaq Play - The most ROI generative “rebrand” in recent history

Let's start with a question - Which sector do you think has attracted the most inflows in the US year to date?

Energy would be the intuitive answer, perhaps followed by Defence. Few would have guessed Consumer Staples to be second, but that's exactly where the data points.

The Consumer Staples sector has seen huge inflows YTD

Source: Intropic

N.B. Net Flows Data in $mn and includes ETF flows just for R1000 constituents

It only takes a matter of seconds to find the driver behind this: Walmart. A surprising result, given the current geopolitical backdrop. What's drawing a disproportionate amount of capital into Walmart when markets are preoccupied with an escalating conflict in the Middle East?

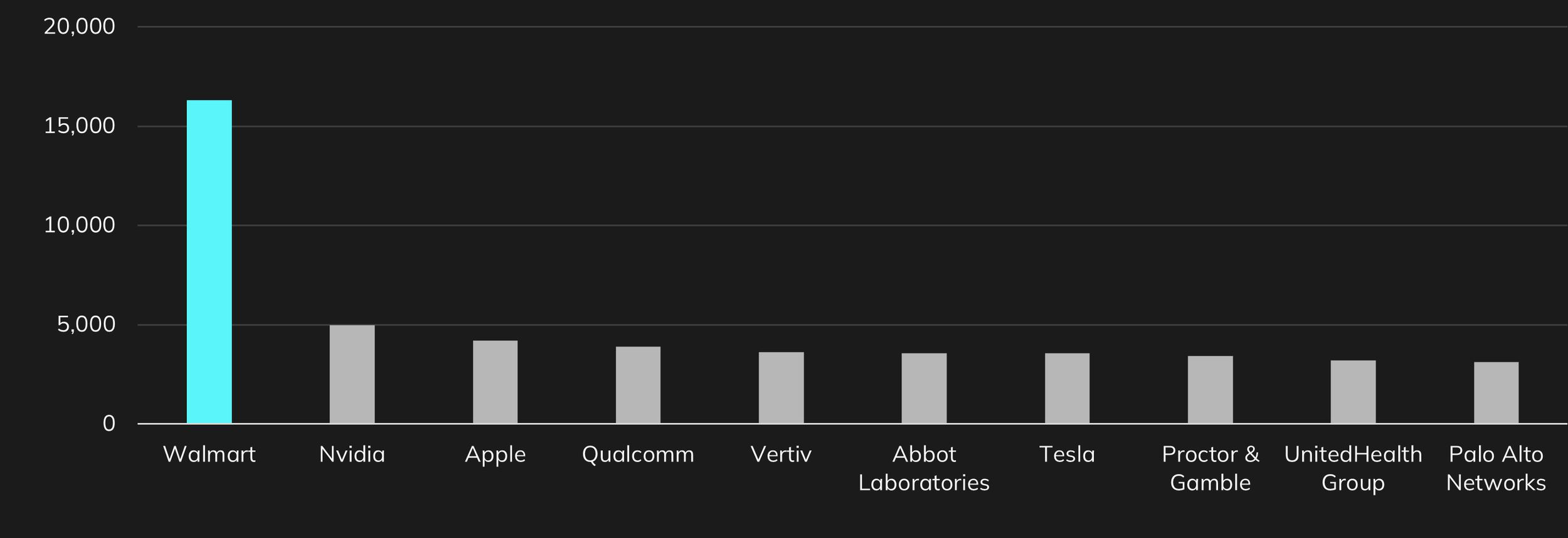

Walmart has driven the overwhelming majority of these flows

Source: Intropic

N.B. Data in $mn and includes ETF flows just for R1000 constituents

To answer this, it helps to take a step back and consider the structure of today's market. As we highlighted in our previous article, in the US, passive funds now account for >53% of assets under management. A key consequence of this is that market flows are increasingly dominated by passive investors, who gain exposure to individual stocks through ETFs and other index-tracking vehicles.

In short, index funds have become a powerful force in directing capital, and as a result, changes to the underlying indices can trigger substantial flows into individual names.

So - what’s been driving Walmart's flows?

In Nov 2025, Walmart announced the transfer of its common stock listing to the Nasdaq, framing the move as an alignment "with the people-led, tech-powered approach" to its long-term strategy.

A creative take on corporate repositioning, and arguably one of the most ROI-generative in recent memory.

The move opened the door to inclusion in the Nasdaq-100 (NDX), which alone stood to drive c.$22 billion in passive demand for Walmart shares, or 8x ADV in a single day.

Once the relisting from the NYSE to the Nasdaq was announced, informed rebalance desks began positioning ahead of the anticipated NDX addition. On January 9, 2026, Walmart was confirmed as AstraZeneca's replacement in the NDX, with the rebalance completing on January 16th.

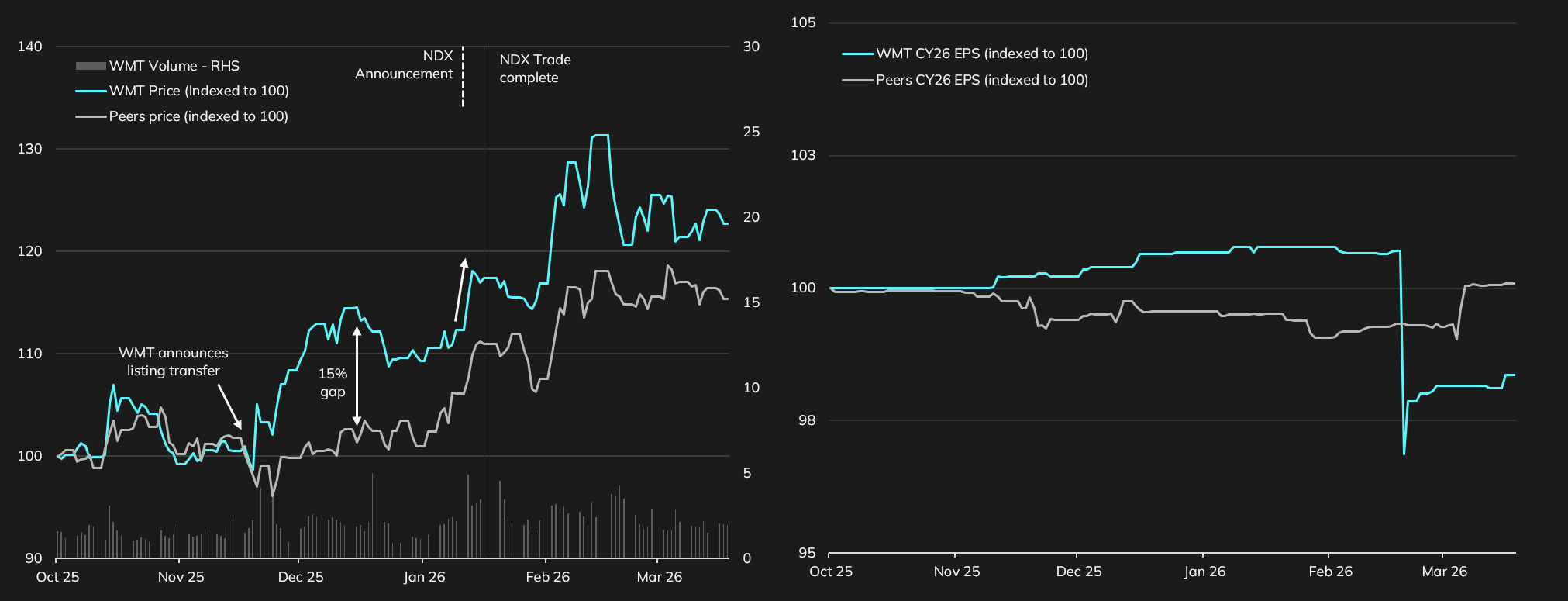

Walmart has outperformed its peers since announcing its listing transfer, despite EPS underperformance

Source: Intropic

The charts above tracks Walmart's price and EPS performance over the past six months against its peers. Over this period, Walmart has outperformed its peer set by more than 15% at times, despite actually underperforming from an EPS forecasts standpoint.

This raises an interesting question from a market efficiency perspective. The Efficient Market Hypothesis suggests that market cap expansion should not be driven mechanically by flows. If capital inflows into a stock are anticipated, arbitrageurs should step in, prices should adjust minimally and temporarily, and equilibrium should be restored.

A deeper look at the divergence away from fundamentals

In the build up to index events (or any event that sees immediate passive flows), we often see a dislocation between fundamental performance of a company, and how this is reflected in the share price.

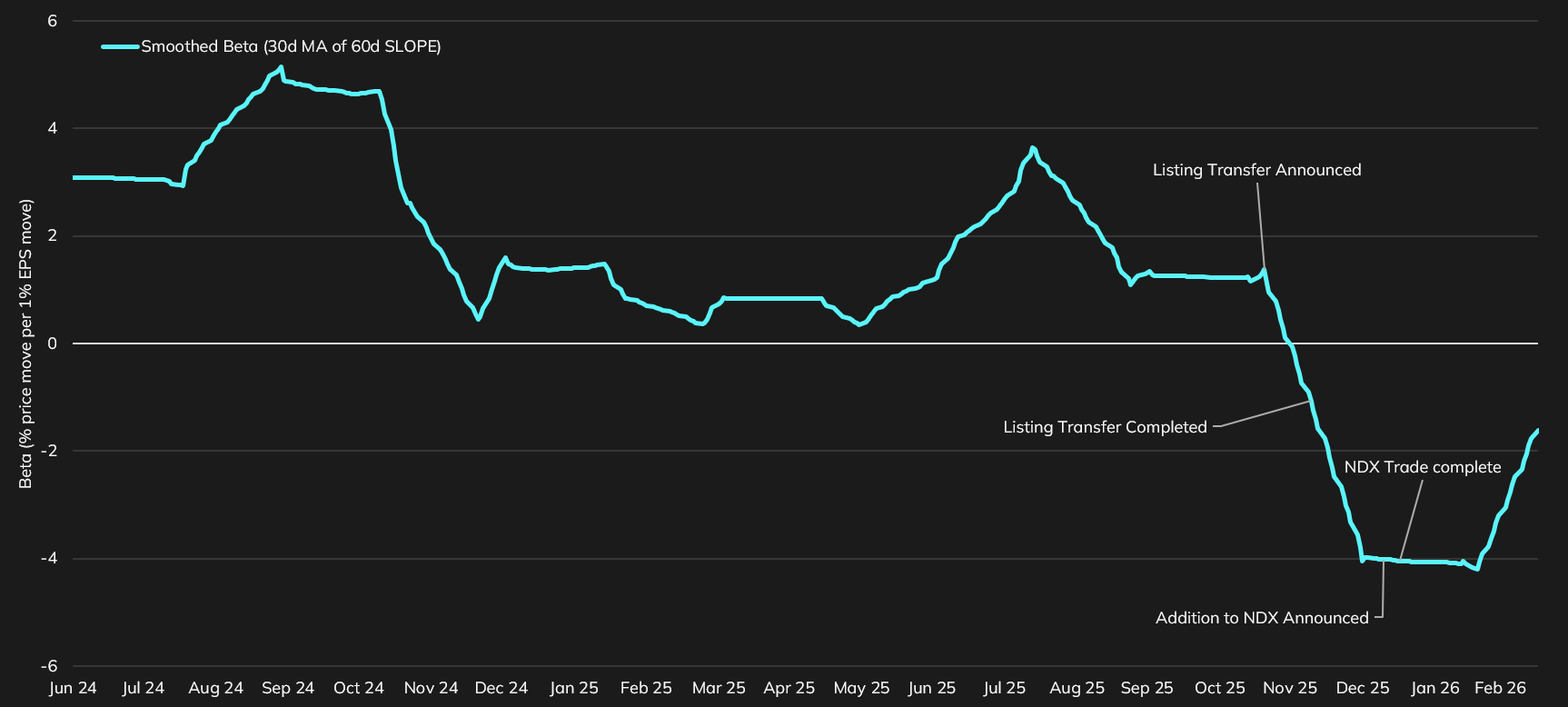

The best way to show this is by running a beta sensitivity test (which shows the sensitivity of share price move per 1% EPS move). As logically expected, historically, when EPS forecasts improve by 1%, share prices also improve (ranging from 0 to 5 depending on the extent of the surprise).

However, when Walmart’s listing transfer was announced, this dynamic completely broke. Over the period of sizeable passive inflows, the share price no longer accurately reflects changing fundamentals.

Price change to EPS sensitivity has completely collapsed since the listing transfer

Source: Intropic

What is the market doing about this?

One of the most notable developments is that Walmart's short interest has surged. Since the relisting announcement, short interest has multiplied nearly 3x, an absolute increase of c$7 billion.

A comparison against peers confirms that this uplift is Walmart-specific, with the increase coinciding closely with the index transition announcement, suggesting the short interest buildup is directly linked to the passive flow dynamics at play.

Walmart short interest has spiked

Source: Intropic

Walmart is not an isolated case, definitely and won’t be the last

This is not the first time a listing transition has been used to capture passive flow dynamics. When Palantir moved from the NYSE to the Nasdaq in Nov 2024, a board member publicly acknowledged that the switch would force billions in ETF buying, a post that was later deleted and drew regulatory scrutiny. The same thing happened when Tesla joined the S&P 500.

The broader implication is that as passive-driven market cap expansion takes hold, it creates a self-reinforcing cycle.

These inflated valuations generally feed into corporate actions, where share buybacks become larger and more frequent, and stock-based compensation tend to rise. This happens as the active side of the market can take longer to reprice these stocks back toward fundamentals, particularly in large-cap names.

The importance of being aware

Understanding when index rebalances trigger, quantifying the magnitude of the resulting flows, and identifying which names are most exposed to mechanical demand is becoming an essential layer of analysis. Without it, fundamental investors risk misattributing passive-driven price moves to market consensus, entering positions at structurally inflated levels, or missing the window in which mean reversion is most likely to occur.

As passive ownership continues to grow, these dislocations will only become more frequent, and more consequential.