SpaceX IPO: Game of Flows (Part I)

In this article, we address the current uncertainty surrounding the immediate passive flow implications of the potential SpaceX IPO. This is the first of a multi-part series. In our next article we set out the implications of lock-up related future flows, and how management could look to drive further passive ownership.

TLDR: Total potential passive demand for SpaceX at IPO could reach ~$18–19bn over the first three weeks if all major indices add the stock (assuming a base case ~$1.75trn market cap at IPO, and ~$75bn free float). This is already below most current media estimates and likely represents an upper bound, as not all indices may ultimately include it.

Introduction

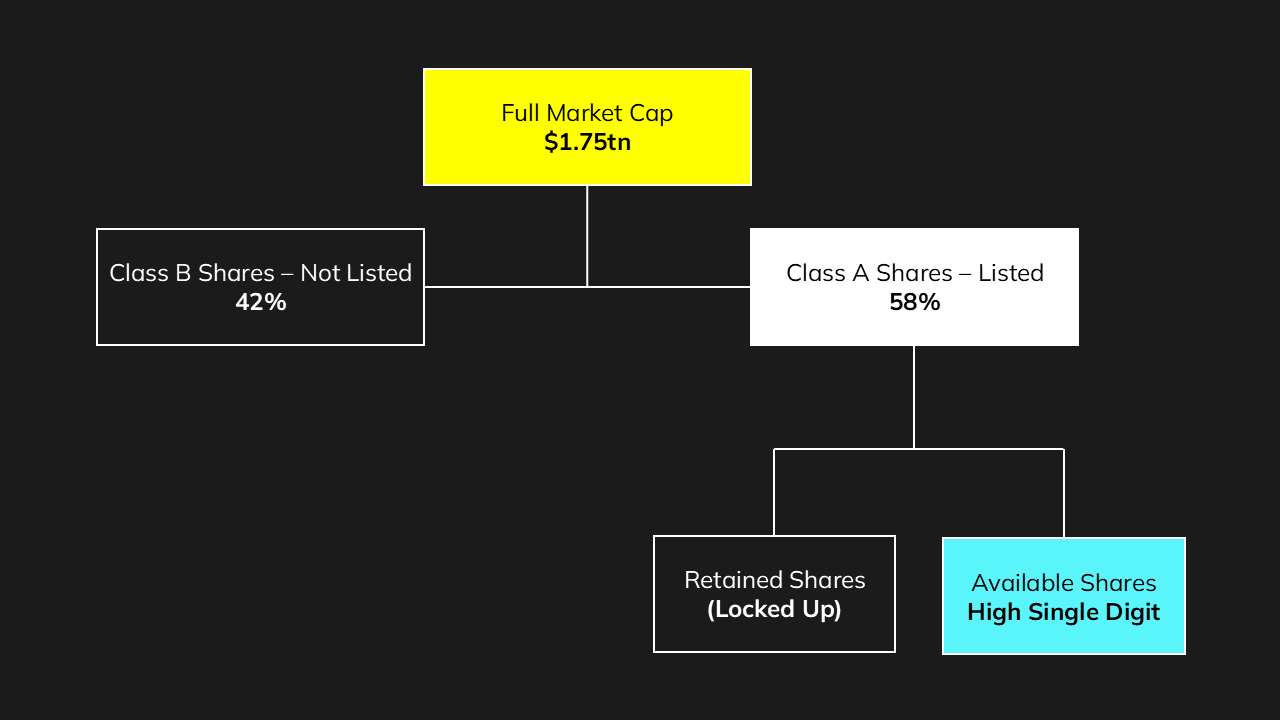

SpaceX is targeting an end-of-June Nasdaq listing at a company market cap of $1.75-2.00tn, with an IPO offer size of c$75bn. Based on public estimates of Elon Musk's ownership stake at 42%, we assume a dual class listing with 58% listed as Class A and Musk’s 42% remaining unlisted as Class B.

SpaceX IPO: Share structure and available shares (%)

Source: Intropic

The IPO comes with unusually high planned retail allocation and months of intense media coverage, a combination that will likely see demand far outstrip supply in early sessions, with daily volumes likely pushing well above the sub-$1bn baseline we would ordinarily expect.

Passive flow impacts: Addressing the inflated market expectations

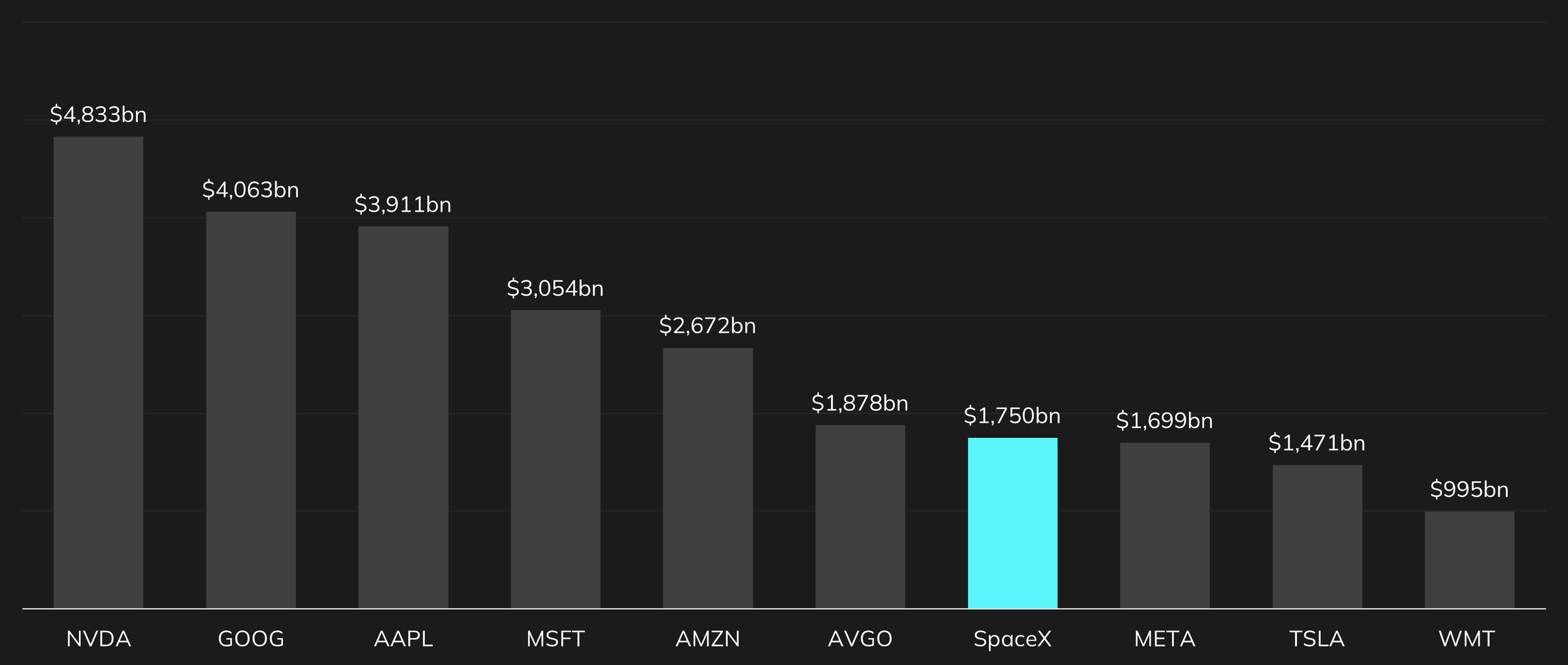

An IPO of this scale has inevitably drawn the attention of major index providers, with some of them recently amending their methodologies to allow for faster entry into their indices. For example, Nasdaq 100 now allows the inclusion of recently IPO-ed stocks on an expedited basis if their full market cap ranks within the top 40 of existing constituents after seven days of trading. At an assumed market cap of $1.75 trillion, SpaceX would comfortably clear that bar, ranking within the top 10 of the index, making Fast Entry eligibility essentially a given under the new rules.

Nasdaq 100: SpaceX among the top 10 on market capitalization basis

Source: Intropic. Data as of 16 April 2026.

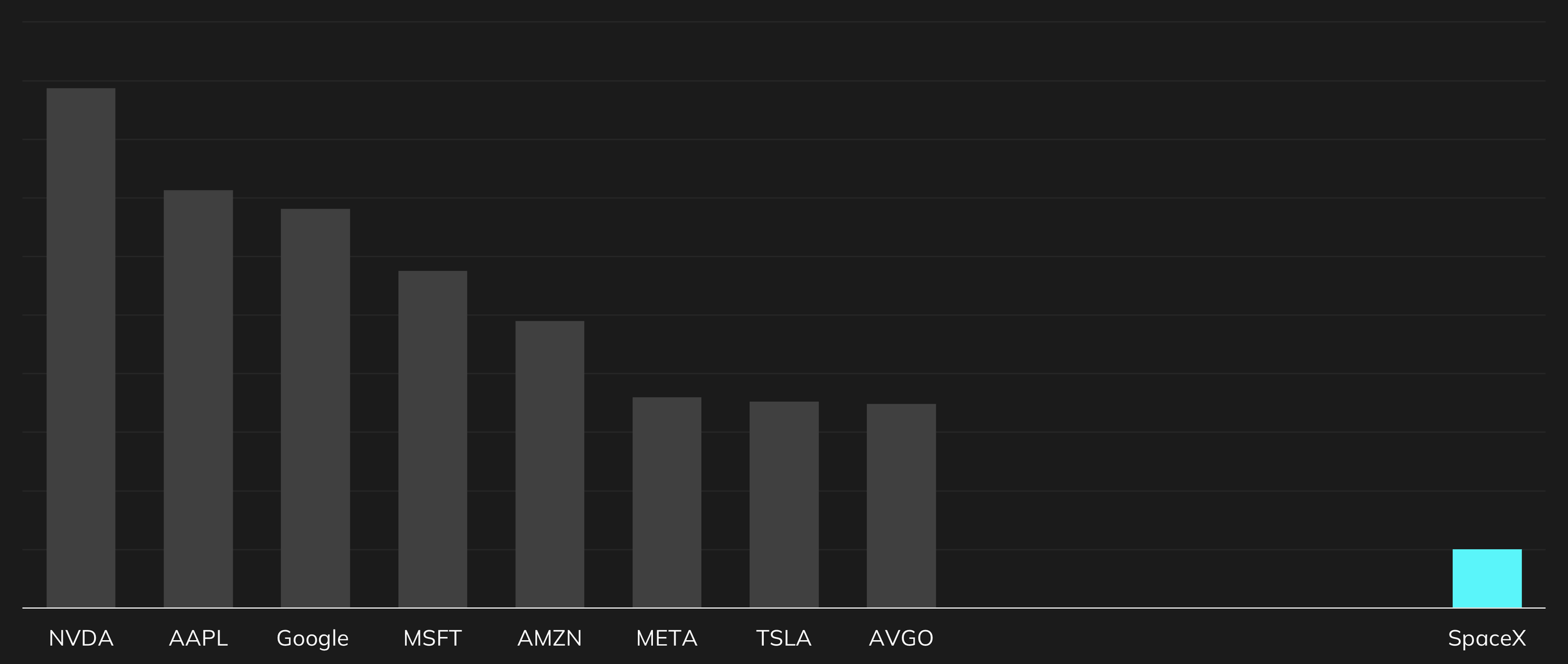

A common misconception we are seeing among investors is the assumption that this ranking automatically translates into a top-tier index weight from day one. On the contrary, the Nasdaq 100 will assign weights based on a modified market capitalisation, which utilises the listed class and free float (in the case of low-float companies such as SpaceX). It means that the dual-class structure and the high-single-digit (%) available shares materially reduce the market capitalisation that Nasdaq actually uses for index weighting. The index provider will determine the precise entry weight through its Weight Interpolation Process, linearly interpolating between neighbouring constituents, placing SpaceX in the first quartile.

Nasdaq 100: SpaceX is far away from the top 10 on modified market cap basis

Source: Intropic. Data as of 16 April 2026.

Ultimately, what this means for passive flows:

Various sources quote a wide variety of forecasts for the passive demand that could come about as a result of index inclusion. We have seen some ambitious estimates, with those at the top end missing out the fact that most indices look at float cap rather than market cap.

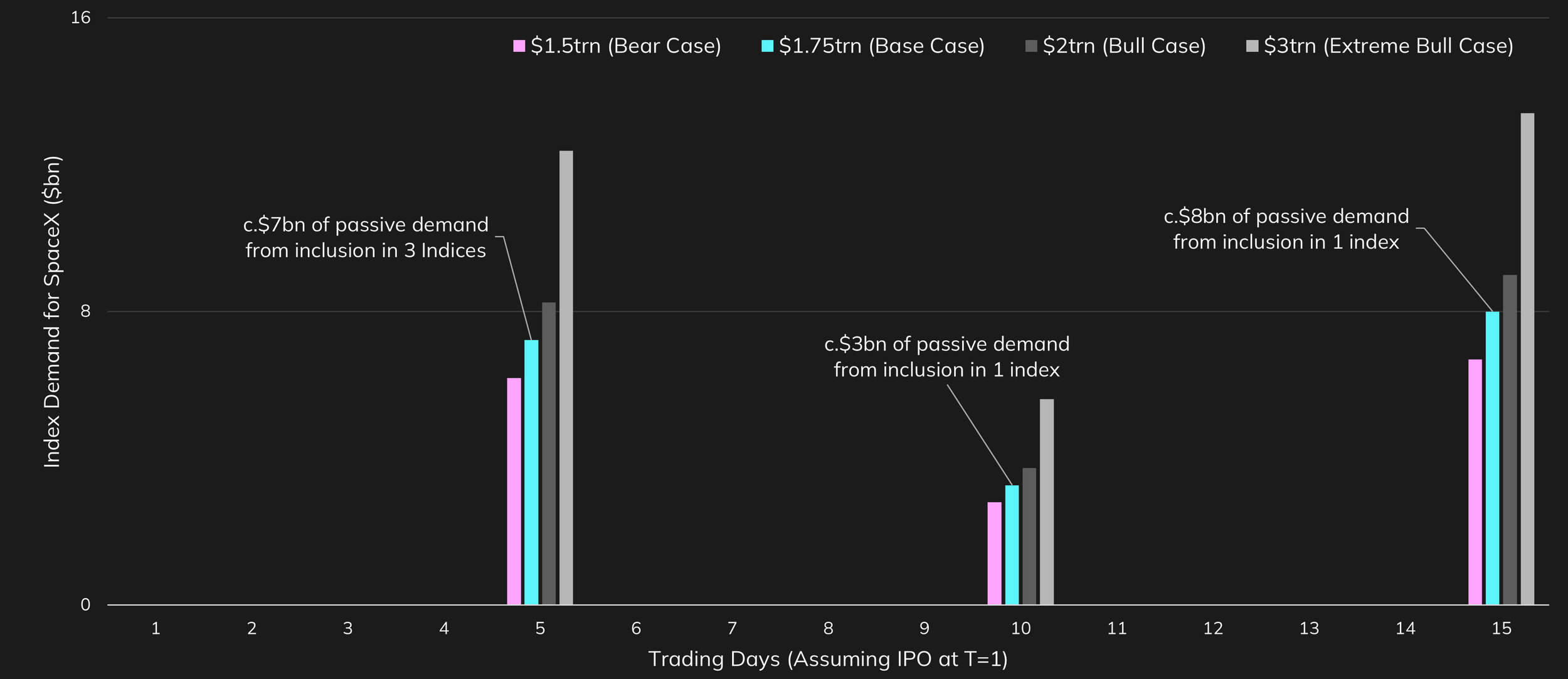

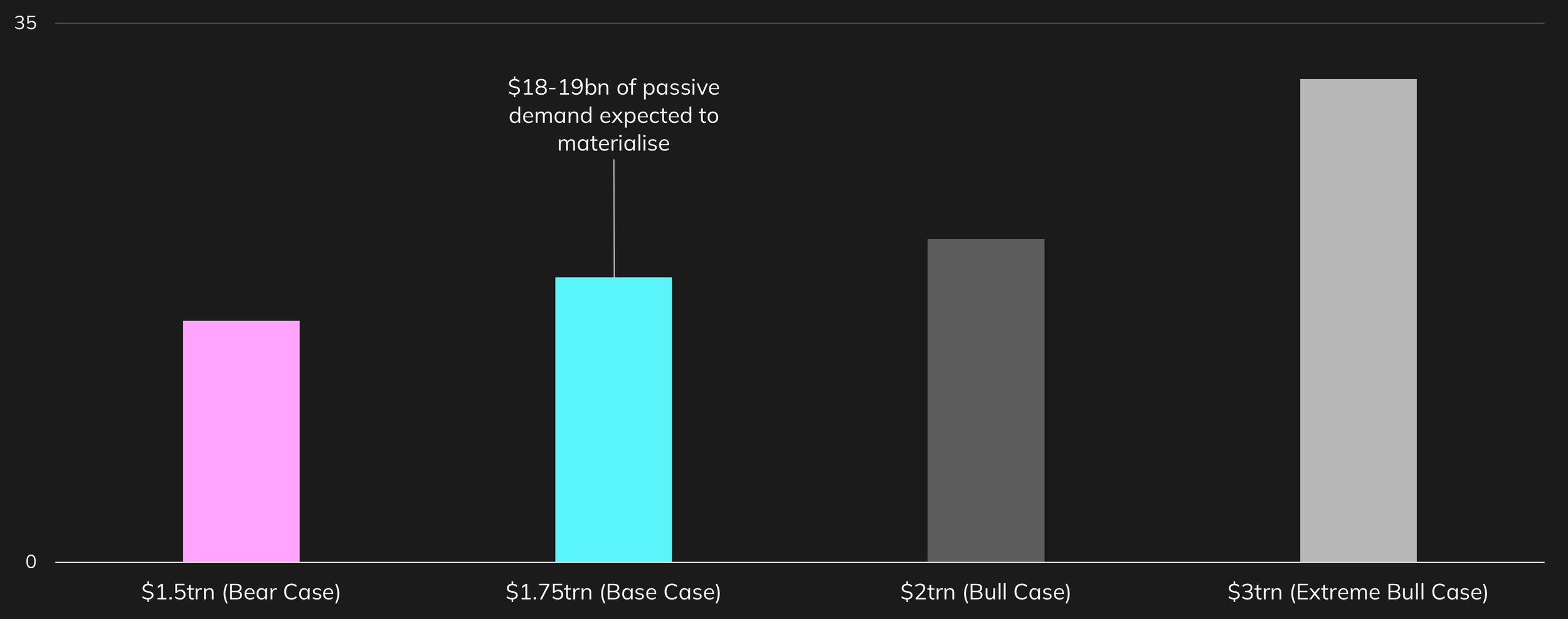

At a consensus market cap of $1.75trn, our base case models c.$18-19bn of total potential passive demand to materialise within 15 trading days, reflecting inclusion across the major cap weighted indices. Timing will vary, with flows materialising at different points post-IPO depending on index-specific methodologies.

The cadence of passive demand from major US indices

Source: Intropic

We assume four valuation scenarios based on day-one trading performance: a $1.5tn bear case (~15% decline), a $1.75tn base case (flat), a $2tn bull case (~15% upside), and a $3tn extreme bull case (~70% upside), with market cap then holding at those levels over the following week. These scenarios drive varying levels of passive demand.

Aggregate passive demand over the first 15 trading days is sizeable

Source: Intropic

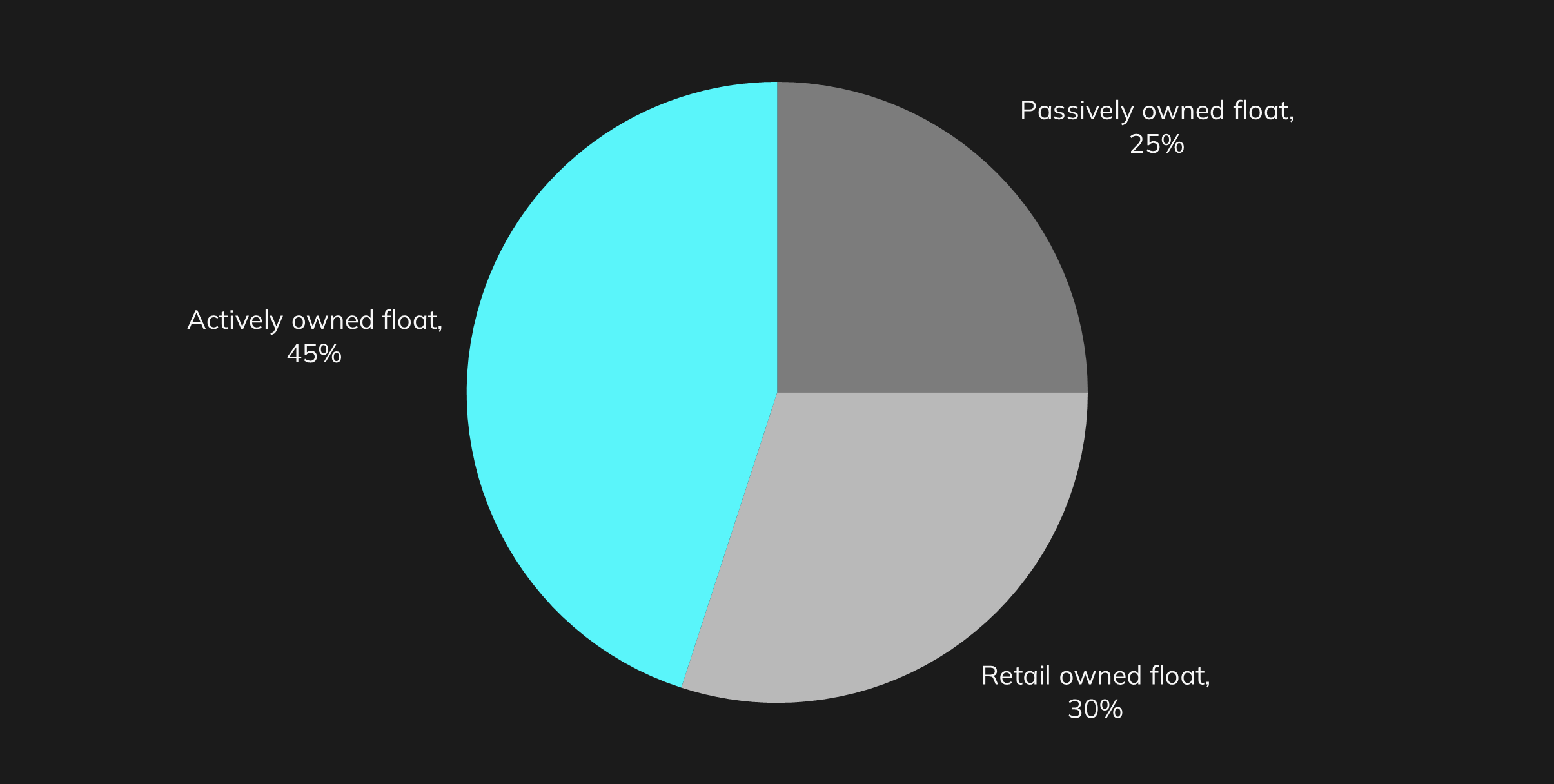

Index inclusion and retail participation materially reduces the “active” free float of the company. We forecast that total passive ownership will make up c25% of free float within the first 15 days of trading, which would put the active share <50%.

Active ownership will likely make up <50% of the float within the first three weeks

Source: Intropic

Mag7: No near-term impact

For investors concerned about what SpaceX's Nasdaq 100 entry means for the Mag7, the near-term answer is: less than you might expect. Because index weight is driven by modified market capitalisation, SpaceX will enter the NDX with a modest weight that displaces existing constituents only marginally. The Mag7 names, which collectively constitute >30% of the index weighting, are unlikely to see meaningful passive selling on the back of the addition alone.

Furthermore, SpaceX’s inclusion into an index like the Nasdaq-100 does not mean a company will be immediately deleted as a result. In fact, its inclusion would mean that the number of companies within the ‘Nasdaq-100’ will, for a time, become 101 companies. That is until the Annual Reconstitution event in December, where the index will reset back to 100 companies. For the other major US indices, there will also be no deletion as a result of a SpaceX inclusion.

The more important story, however, may play out over the months that follow. As lock-up periods expire post-IPO, the available shares will gradually increase, and with it, SpaceX's modified market cap and its index weight. Each step up translates directly into a larger index footprint, which means the passive selling pressure on existing constituents, including the Mag7, builds over time rather than arriving in one concentrated event.

SpaceX management will already be familiar with this process, and in our next article we set out how we expect these flows to unfold.

Assumptions

Intropic has used the following assumptions in its forecasts:

Company market cap: $1.75trn

IPO offer size: $75bn

IPO date: End of June

We have also assumed that SpaceX will have two share classes with the split based on Elon Musk’s ownership stake:

58% Class A, which is listed

42% Class B, which remains unlisted