The Rise of Passive

Part 1 of 3

From fringe idea to market dominance

Let’s start from the beginning. The first investable index fund launched in 1971. However, it’s in 1993 that we started to see a shift in market behaviour, with State Street launching SPY, the first major ETF tracking the S&P 500. It started with just $6.5 million in assets and crossed $1 billion within three years.

From there, each decade brought a new accelerant. The late 1990s internet bubble pulled retail investors into markets, many of whom chose index funds as the simplest entry point. The early 2000s brought SPIVA scorecards, which quantified something many suspected: most active managers underperform their benchmarks over time. Changing pension regulations pushed institutional capital in the same direction. By the 2010s, demand had reached the scale where costs collapsed; Vanguard, BlackRock, and others drove expense ratios toward zero, making the value proposition almost impossible to argue against. More recently, the SEC's standardisation of ETF approvals has supercharged supply. The number of US ETFs has grown from 1,716 in 2017 to 4,402 by the end of 2025. In 2023, passive AUM surpassed active in the US for the first time. Globally, passive continues to gain market share, and at the current pace, it's likely to overtake active investing within the next few years.

Passive AUM has now surpassed Active AUM in the US

Source: Intropic, Research Affiliates and Morningstar

N.B. Data includes U.S. open-ended funds and ETFs (with obsolete funds included)

Where are the flows going today?

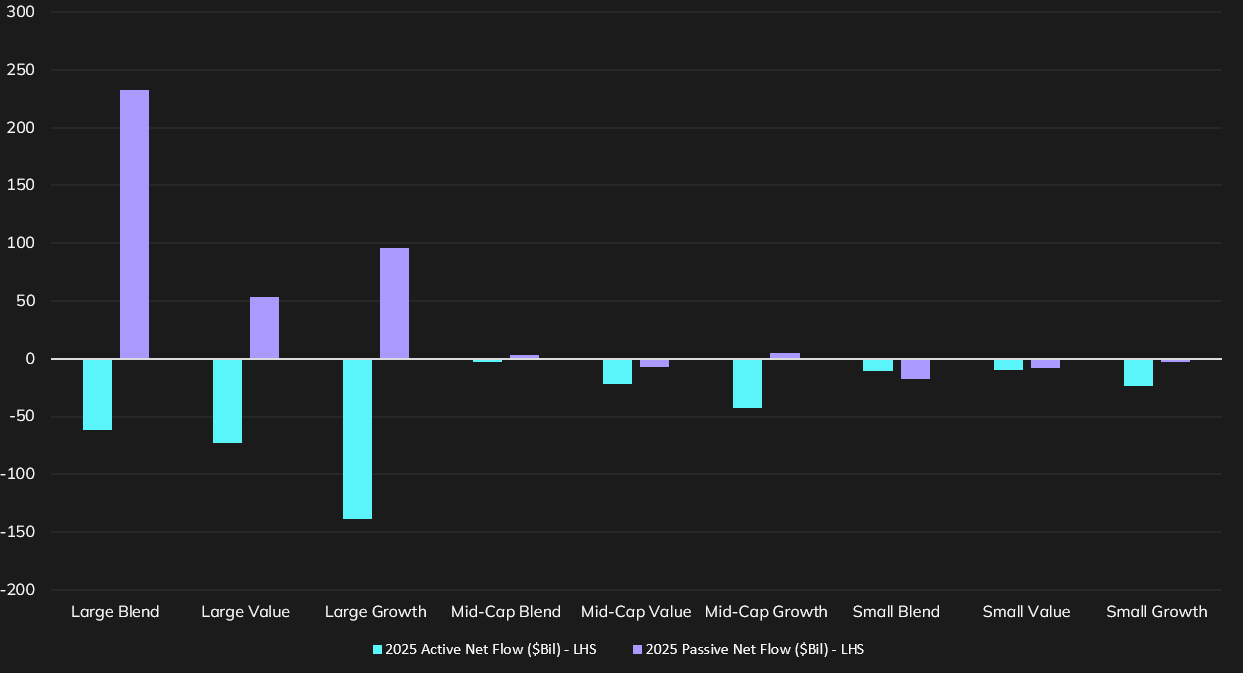

The rotation towards passive is ongoing, and accelerating in specific segments. Over 2025, US active equity funds saw net outflows of -$32.3 billion, led predominantly by the large-cap segment. Mid-to-small cap funds saw outflows across both active and passive, as investors doubled down on large-cap exposure amid the continued strength of mega-cap tech. Heading into 2026, one development worth watching is the rise of active ETFs, actively managed strategies delivered in an ETF wrapper. These offer the liquidity, transparency, and tax advantages of the ETF structure while retaining discretionary portfolio management. It's worth noting that retail investors now account for 75% of US ETF assets, up from 56% a decade ago.

US Equity fund flows over 2025 show significant active outflow & passive inflow in large cap stocks

Source: Morningstar

Why this matters

None of this is new information in isolation. But the cumulative scale of this shift is what makes it consequential. When passive funds hold 30%+ of the float of the largest stocks in the world, and when the vast majority of net new capital flows into index-tracking vehicles, the mechanics of how stocks are priced fundamentally change.