The Narrowing Edge: Why Active Managers Are Struggling

Part 2 of 3

The underperformance problem

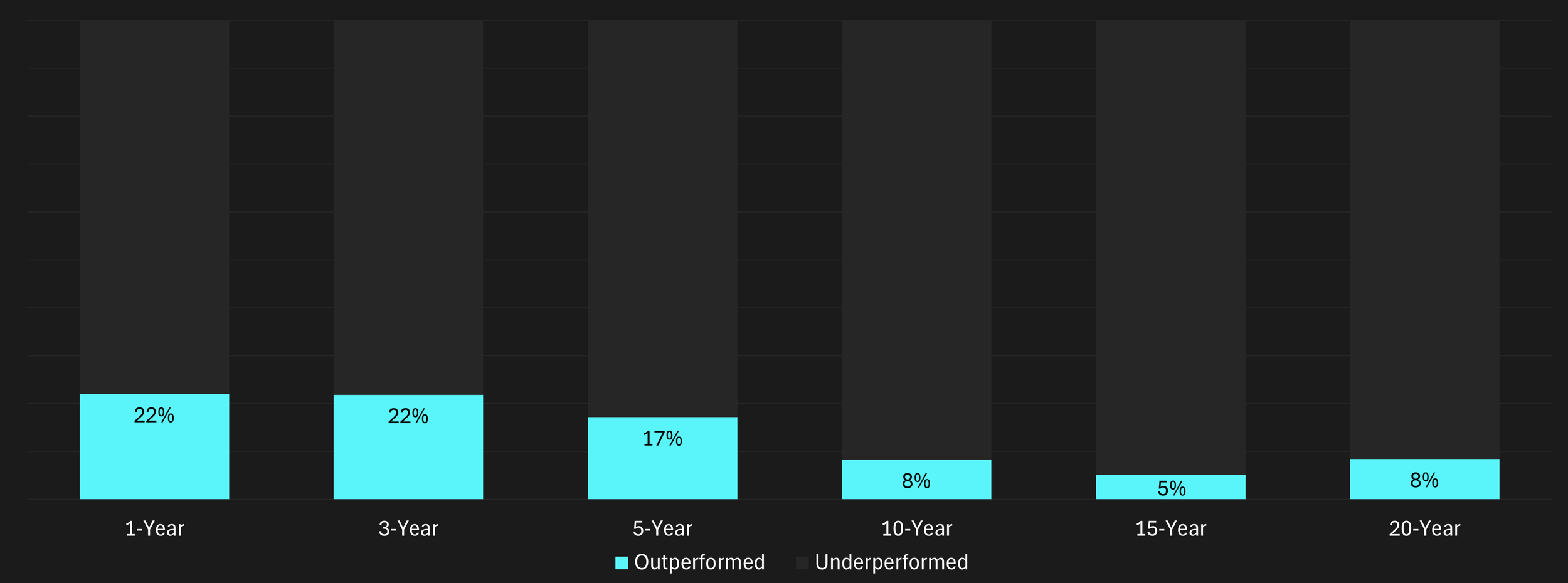

Let's start with the numbers. Looking at US Large-Cap Blend Equity as of mid-2025, 78% of active managers underperformed their passive equivalents over a one-year horizon. Only 22% generated excess returns. And the longer you extend the window, the worse it gets: underperformance rates reach 78–92% over three-, five-, and ten-year periods, and remain elevated over fifteen- and twenty-year horizons.

US Large-Cap Blend Equity’s active survived funds performance

Source: Morningstar, Intropic. Data as of June 2025

The consequences are existential for many funds. Persistent underperformance drives outflows, which erode economies of scale and operating viability. By mid-2025, 6% of active funds had been closed or merged within the prior year. Over three years, that figure rises to 16%. Over five years, 25%. And over a decade, nearly half (47%) of active funds failed to survive. Over twenty years, the non-survival rate reaches 73%.

The passive tracking factor

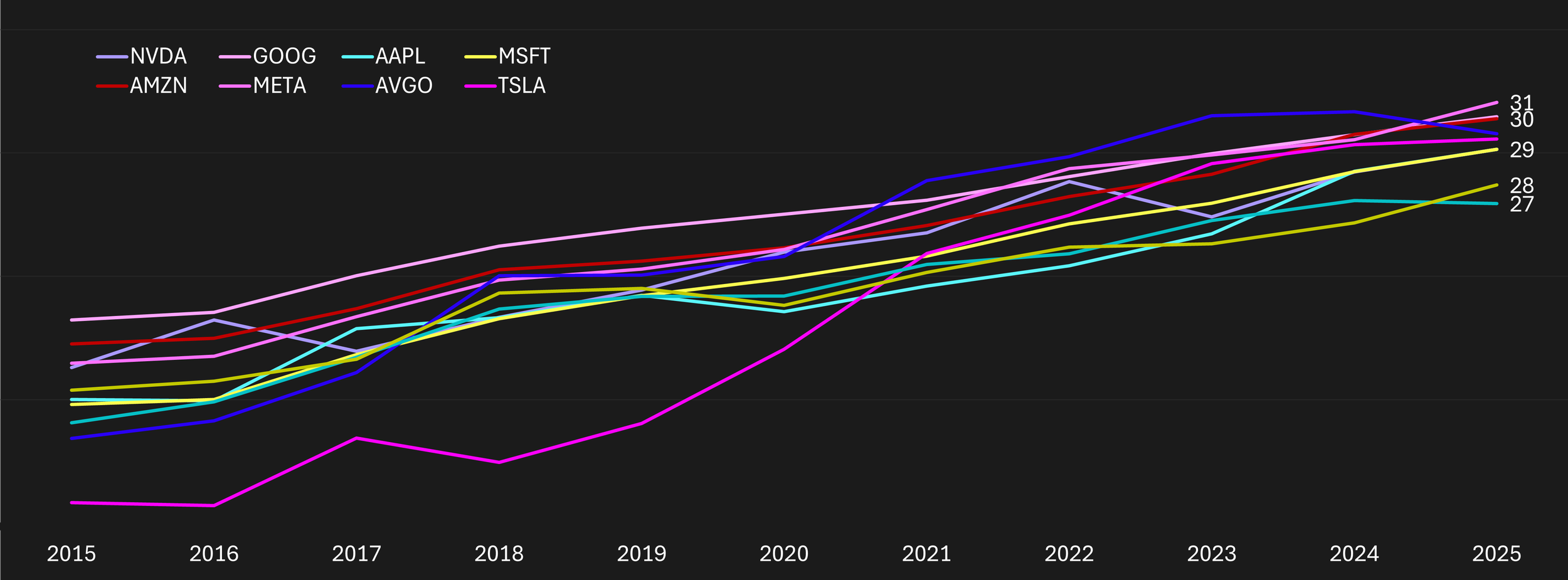

To understand why, it helps to look at what's happening at the stock level. One of the reasons is that the share of float held by passive funds in the ten largest US stocks has grown to 30% in 2025. That's a substantial share of the ownership base that allocates capital mechanically, based on index weights, not fundamental views.

Share of passive ownership across top 10 US stocks

Source: Intropic. Note: Percentage of ownership.

At this level of penetration, passive ownership becomes a structural feature of how these stocks trade. Every dollar flowing into an S&P 500 ETF gets distributed across constituents based on their index weight. The largest stocks receive the largest share of inflows, reinforcing their weight, which in turn attracts more capital. It's a self-reinforcing loop, and it operates independently of whether those companies' fundamentals justify the incremental demand.

For active managers, this creates an asymmetry. A correct fundamental view on a stock can still underperform if that stock isn't a major beneficiary of index-driven flows. Conversely, stocks that are heavily weighted in major indices can continue to outperform even as fundamentals soften, simply because the flow dynamics support them.

Stock picking becomes more difficult

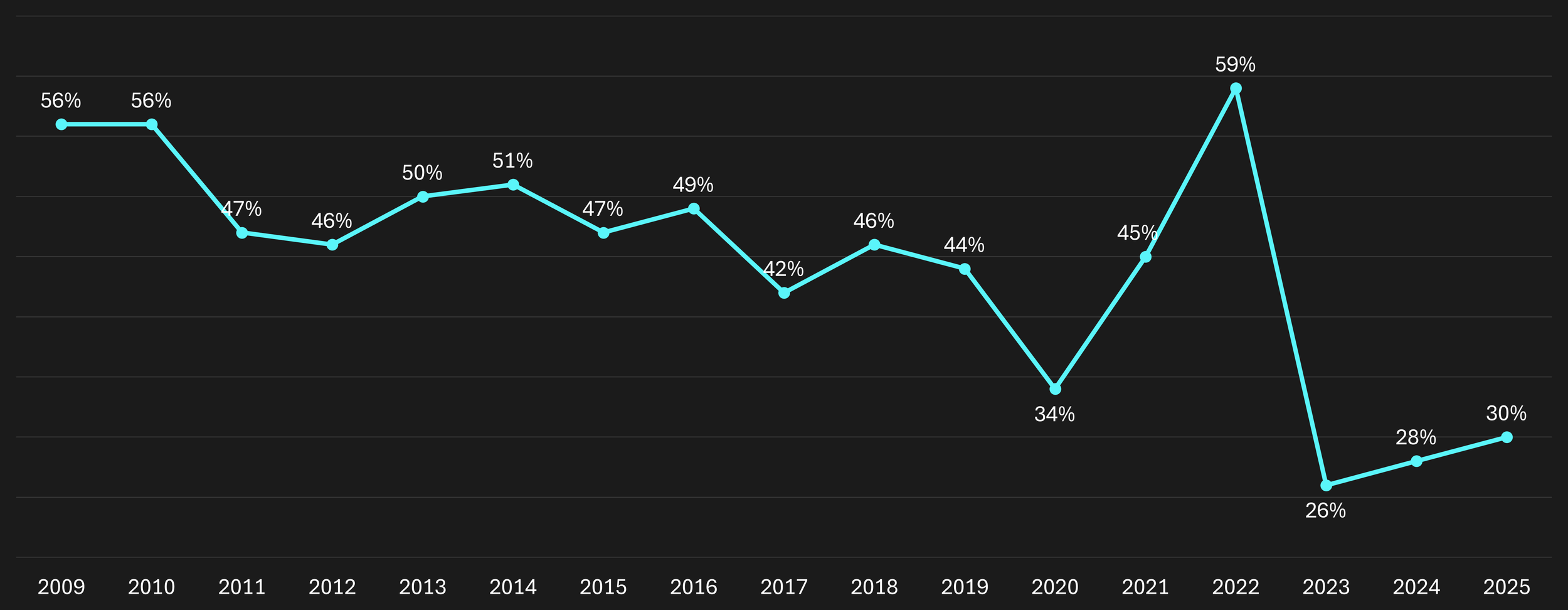

This dynamic shows up clearly in market breadth. In 2009, more than half of S&P 500 constituents outperformed the index. That proportion has trended steadily lower, falling to 34% in 2020 and reaching just 26-30% in 2023-2025.

Percentage of S&P 500 constituents beating the index performance

Source: S&P Global, Intropic.

Think about what that means in practice. If you're an active manager running a concentrated portfolio of 30-50 stocks, and only a quarter of the index is outperforming it, you need to be right on a disproportionate number of your positions just to keep up. The probability of success has shifted against you, not because your research is worse, but because the index itself is being driven by a narrowing set of stocks that benefit most from mechanical capital flows.

In other terms, fundamental analysis became insufficient on its own. The benchmark you're measured against is increasingly shaped by flows rather than fundamentals, and if you're not accounting for that, you're fighting a structural headwind.

What comes next

The evidence so far tells us that active managers are operating in a harder environment, one where passive concentration compresses breadth and reinforces the dominance of the largest index constituents. But this raises a deeper question: is this underperformance caused by a change in the market microstructure?