A Different Market Microstructure

Part 3 of 3

What happens when a stock joins an index?

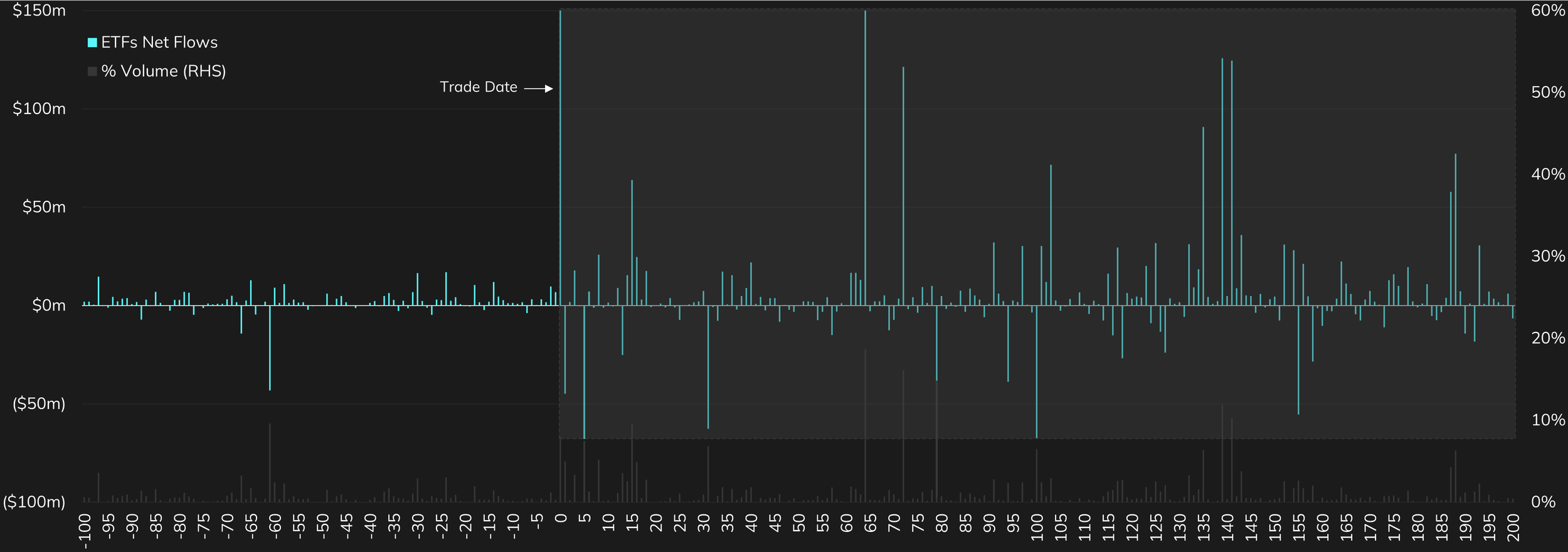

Index inclusion is a defining moment in a stock's trading life. When a stock is added to a major index, it experiences a sharp and sustained increase in flow-driven activity. Our study on S&P 500 additions shows that ETF-related trading frequently surges to account for more than 10% of total volume in the periods surrounding and following inclusion. The stock transitions into a different trading regime, one where liquidity, volatility, and short-term price dynamics become increasingly shaped by index-linked demand rather than incremental fundamental information. This is only a part of the passive pressure as we are not including other index-linked funds (eg. index-linked mutual funds).

ETF Flows in newly added stocks to the S&P 500

Source: Intropic. Average of a sample size of 15 S&P 500 additions from 2022 to 2024. Trade date = day the stock gets included into the index.Higher passive ownership leads to higher volatility

The above inflow of passive capital leads to a change in ownership structure. Investors such as Bill Ackman have argued that shares held by investors through passive strategies actually means that the true float of a company shrinks. As a result of this, more power is placed on the marginal buyer/seller of shares, which can lead to larger gyrations in prices, the lower the true float becomes. In essence, companies which are increasingly being held passively are seeing growing levels of volatility.

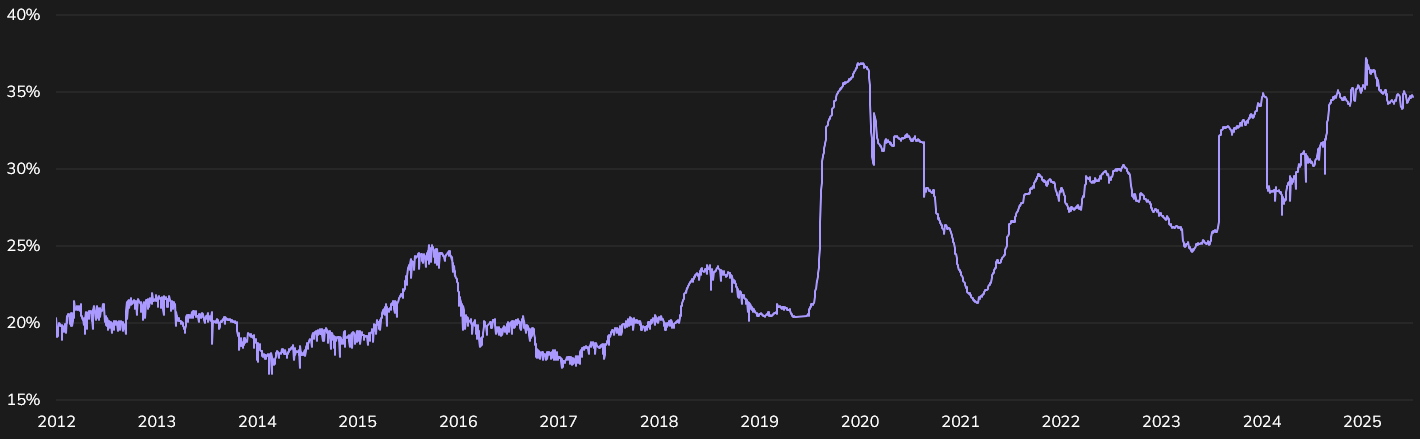

We conducted a study on the volatility levels of the current S&P 100 constituents, focusing specifically on their factor-neutral volatility. The results show that this has nearly doubled over the past decade, suggesting that it is not simply a cyclical phenomenon, but a structural shift in how equities trade in an increasingly passive market.

Factor-neutral volatility has grown over time

Source: Intropic. Note: Realised factor-neutral volatility annualised using a 126-day rolling windowAs passive ownership rises, fundamentals play a smaller role in price formation

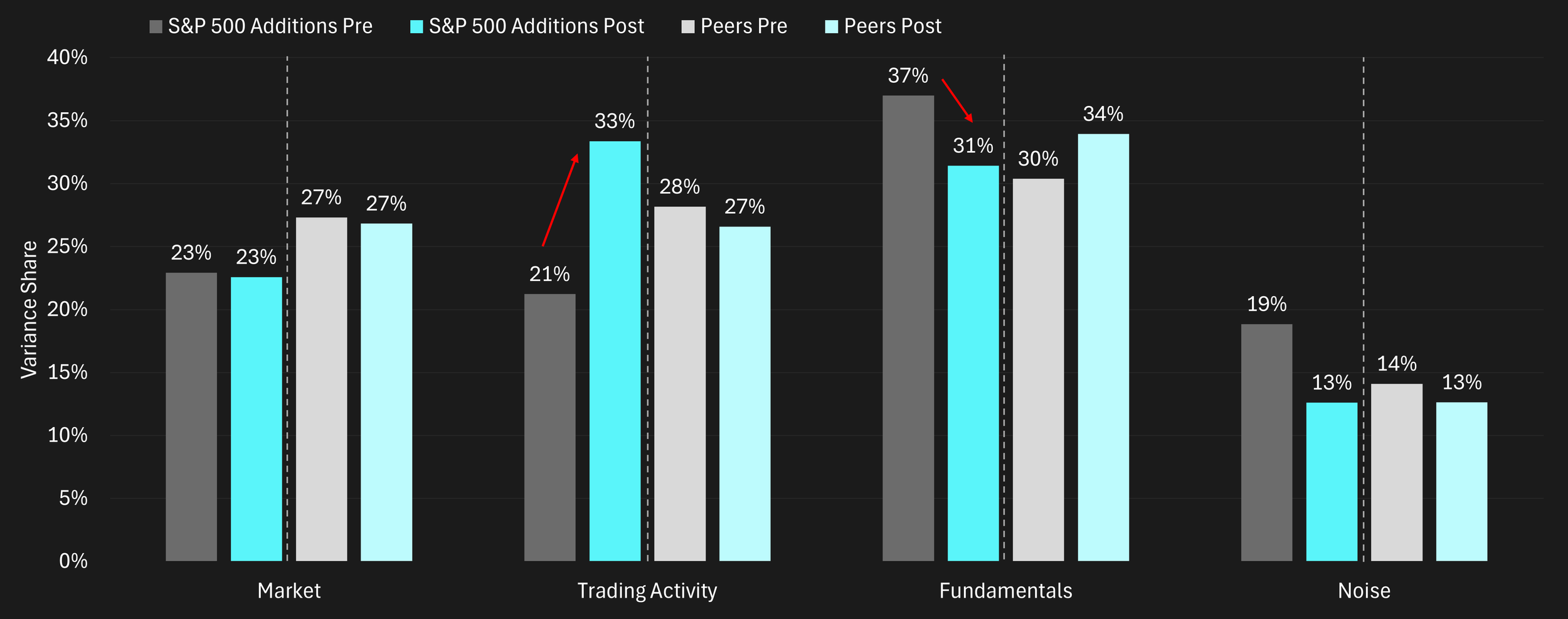

The increase in volatility levels leads to a deeper question: what happens to the role of fundamentals as passive ownership rises? To answer this question, we analyzed S&P 500 additions during 2020–2024 using a ±250 trading-day event window around each inclusion date. For each stock, we applied a return-variance decomposition, which separates total return variance into four components based on how price movements are transmitted: (1) Market-wide information, (2) Mechanical flows or trading activity, including passive and private information flows, (3) Fundamentals, and (4) Noise.

We performed this decomposition separately before and after inclusion, averaged across a sample of 50 stocks, and compared them to a matched set of peer firms that were not added to or were part of the index.

Our findings show that post-inclusion, added stocks see a material rise in the share of variance attributed to trading activity, accompanied by declines in fundamentals. Prices become less directly linked to fundamentals and more dependent on order flow.

Variance decomposition of S&P 500 addition pre- and post-index inclusion

Source: Intropic. Note: Sample size of 50 S&P 500 additions from 2020 to 2024, and 50 fundamentally-linked peers.

This shift aligns closely with the intuition of Grossman–Stiglitz of stock prices only tracking intrinsic value because a shrinking proportion of investors actively spend resources to discover and trade on fundamental information. If fewer investors do that work, as capital shifts toward passive strategies, less information gets embedded into market prices. This doesn't necessarily imply inefficiency, but it does indicate a reduction in the quality and fundamental anchoring of price movements. For active investors trying to extract signal from fundamentals, the signal-to-noise ratio has deteriorated.

The case of Walmart: $22bn of demand unlocked just from re-listing

Walmart’s re-listing to the Nasdaq from the NYSE is a strong example of how index inclusion can affect even the largest companies. On the 20th of November 2025, Walmart announced it would be changing its listing to the Nasdaq. Whilst the company flagged that the re-listing aligned with Walmart’s “people-led, tech-powered approach,” it also stood to benefit from inclusion in Nasdaq’s NDX — this alone would drive $22bn USD of passive demand for its shares (~8x ADV).

Once the re-listing from the NYSE to the Nasdaq was announced, smart rebalance desks began to position ahead of the imminent announcement that WMT would be added to the NDX. As a result, Walmart’s performance versus peers widened during the pre-inclusion period, with outperformance reaching 15% at its peak. On Jan 9, 2026, WMT was announced to replace AstraZeneca in the NDX, with the trade completing on Jan 16th. Volumes peaked as passive fund demand spiked for shares, with overall the proportion of passive ownership rising by c.3% as a result of the re-listing.

Walmart’s volume and indexed price vs fundamentally-linked peers

Source: Bloomberg, Intropic. Peers include the constituents of the State Street US Consumer Staples ETF (XLP) excluding Walmart and equally weighted.

What this means for active investors

The evidence points to the conclusion that the market microstructure has shifted in ways that are material for anyone running an active equity strategy. Passive ownership hasn't made fundamental analysis irrelevant, fundamentals still drive long-term value. But prices have become less immediately anchored to them. Trade-driven and flow-related dynamics now account for a larger share of price formation, meaning traditional fundamental signals can show weaker alignment with returns over horizons that matter for performance measurement and risk management.

For active managers, this has practical implications. Index-related flows introduce an additional source of risk that doesn't show up in conventional fundamental analysis. Stocks can diverge from fair value for reasons that are entirely mechanical, and those divergences can persist long enough to impact quarterly and annual performance. Conversely, these same divergences create opportunities, but only for investors who can identify them in advance and distinguish flow-driven distortions from genuine fundamental deterioration.

In our view, effective alpha generation in this environment benefits from combining fundamental insight with an understanding of positioning, flows, and market microstructure. The toolkit for active management needs to expand beyond public information and company research, as these are no longer sufficient on their own.