SpaceX IPO: Game of Flows (Part II)

In this article we answer the following questions:

IPO documents have been released and valuation implied. What does this mean for passive flows?

With index providers' fast-entry rules in focus, how much passive ownership could ultimately be created?

How does fast-track index inclusion affect price formation?

Could forced buying and strong retail participation create a reflexive feedback loop in the stock?

What are the implications of price discovery occurring within a constrained free float?

How should investors think about the IPO over the short, medium and longer term?

Introduction

A couple of months ago, we released our initial look at the upcoming SpaceX IPO. Whilst most coverage focused on the scale of the IPO, we took a more targeted look at the passive demand its index inclusion would drive.

Much has changed since. Index providers have passed rule changes allowing mega-cap IPOs like SpaceX to be fast-tracked into indices. Rule changes that have drawn mixed reactions from investors and media alike. IPO terms have also been finalised, confirming a share pricing at $135, with 555,555,555 Class A shares confirmed to be offered (a c.$75bn total offer size). This implies a 7.41% free-float, and a c.$1.75trn valuation for the company.

We continue our analysis of what this will mean for flows.

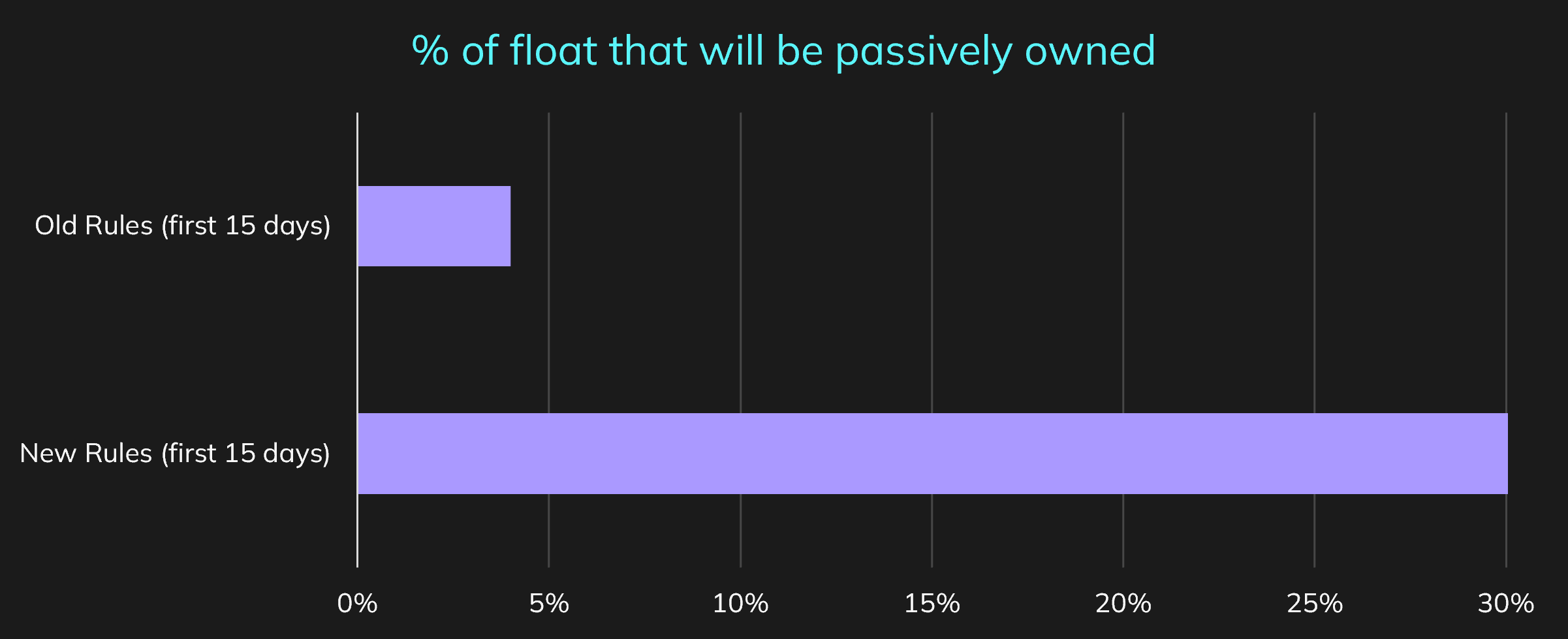

Rule changes push passive ownership to ~30% of float from ~4% originally

Since early 2026, key index providers have run consultations on their treatment on IPO Fast Entry and minimum entry requirements. These changes significantly raise the share of SpaceX’s float that will be passively held, particularly in the first 15 days of trading.

Source: Intropic.

Together, these consultations imply passive ownership will rise to c.30% of float, placing SpaceX among the most passively held large-cap US stocks after just 15 days of trading.

Source: Intropic. Note: passive ownership as a percentage of float.

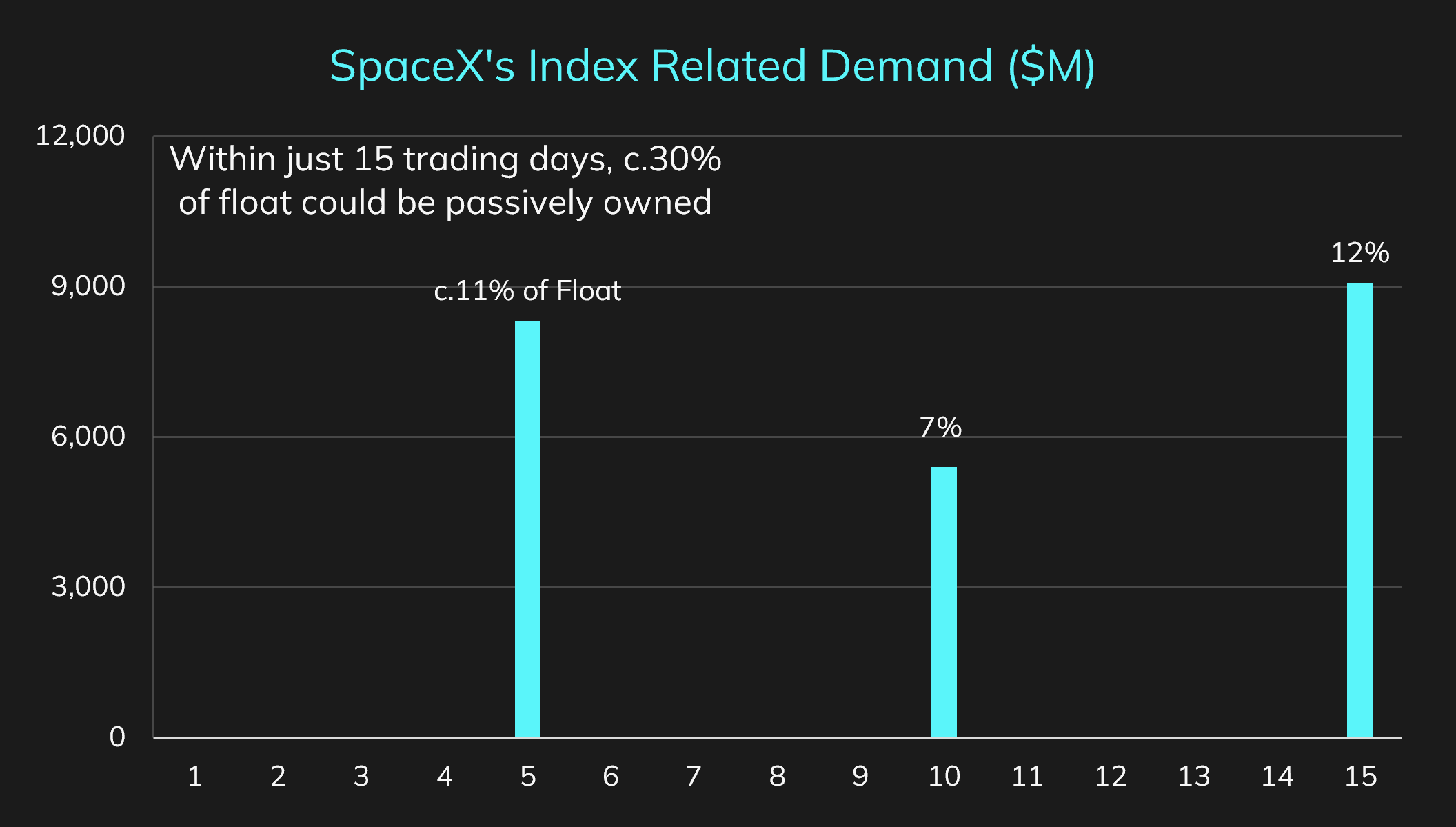

Demand is front-loaded into the first three weeks

Trading during the first three weeks following the IPO is likely to be heavily influenced by periodic demand from index-tracking funds. These concentrated buying events could have a meaningful impact on price formation during the early stages of trading. By the end of the first three weeks, passive investors are projected to own c.30% of the free float, creating a significant source of incremental demand within a relatively short period.

Source: Intropic. Note: index related demand across the first 15 days. Updated post index provider announcement on 10/06/26

Fast-entry flows could drive impact price up to 20%

SpaceX represents a relatively unique IPO case for two reasons. First, its expected market capitalization would make it immediately eligible for some of the world's largest and most widely followed equity indices. Second, major index providers have only recently introduced fast-entry provisions designed specifically to accelerate the inclusion of large IPOs.

Evidence from prior fast-entry events suggests that these rules can have a meaningful impact on both flows and pricing. A study by Marco Sammon and Chris Murray (Harvard Business School) finds that mechanical demand from CRSP-tracking funds averaged c.7% of IPO float and generated an immediate price impact of c.5%. For SpaceX, index-related demand could ultimately represent c.30% of the free float. While the relationship between passive demand and price impact is unlikely to scale linearly, the comparison highlights the potential magnitude of the index bid and its influence on early trading dynamics.

This impact is temporary. The c.5% gain ahead of CRSP addition halves over the following weeks, but clearly matters for pricing in the early stages of the IPO.

The reflexive loop: higher rank-date market cap can lead to larger flows

Index inclusion decisions vary based on methodology. One index ranks float-adjusted market cap on either the first or second day of trading to decide whether inclusion occurs, whilst the another ranks float-adjusted market cap based on the 7th day trading, with this market cap used to calculate the corresponding flows.

As a result, index-related demand is reflexive: the higher the market cap at “rank date”, the larger the passive flow when the stock enters the index. With index desks often prepositioning these trades ahead of rank date (as shown by the 5% price uplift in the study mentioned earlier), this could lead to a situation where a temporarily elevated market cap drives more sizeable passive flows, which resets the passive flows expectations ahead of rank dates.

Passive Demand Expectations at Different Market Cap Levels

Source: Intropic. Note: The feedback loop depends on market elasticity and retail participation; we take no view on fundamental value or active investor positioning.

The reflexive loop can also feed into the IPO price itself. If investors are aware of the short-term price implications, and the shareholder book at early trade is geared toward those looking to capitalise from this trade, then the IPO may price at a level that accounts for these passive flows.

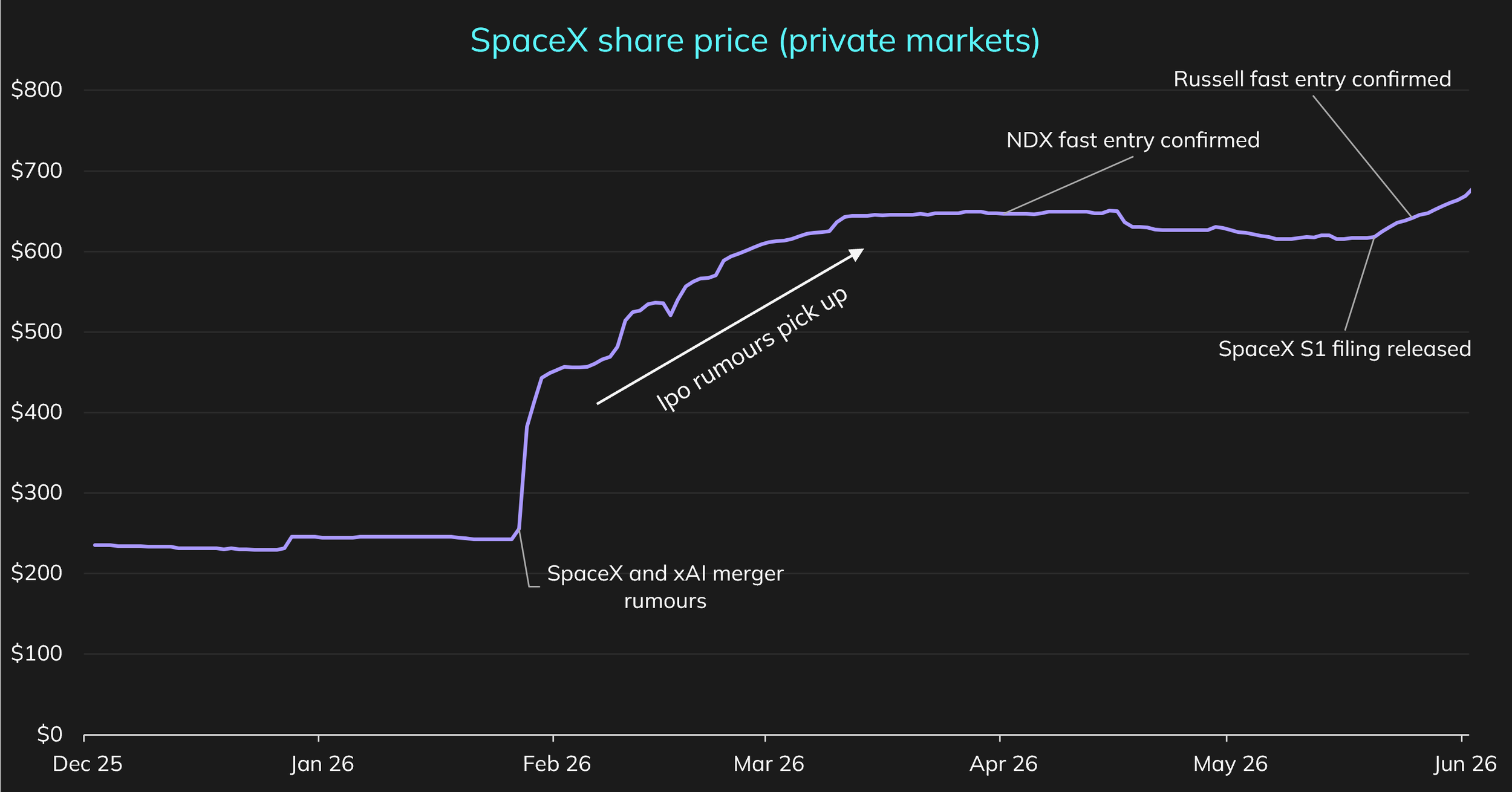

Whilst private market prices have risen, it would seem that much of this jump is related to SpaceX’s acquisition of x-AI, the IPO rumours themselves and the release of the S-1 filing. Prices didn’t move much on the confirmation that SpaceX would be added to the NDX, and the Russell fast-entry confirmation only occurred after the release of the S-1, so the period is too noisy to associate gains with this.

Source: Hiive, Intropic.

If active investors are expected to make up an insignificant proportion of ownership, does price discovery become an afterthought?

The price impact of passive flows is short-lived, but it could disrupt price discovery at arguably the most important point of a company’s stock market journey. The bigger story is structural: SpaceX’s share register looks like no other recent US IPO.

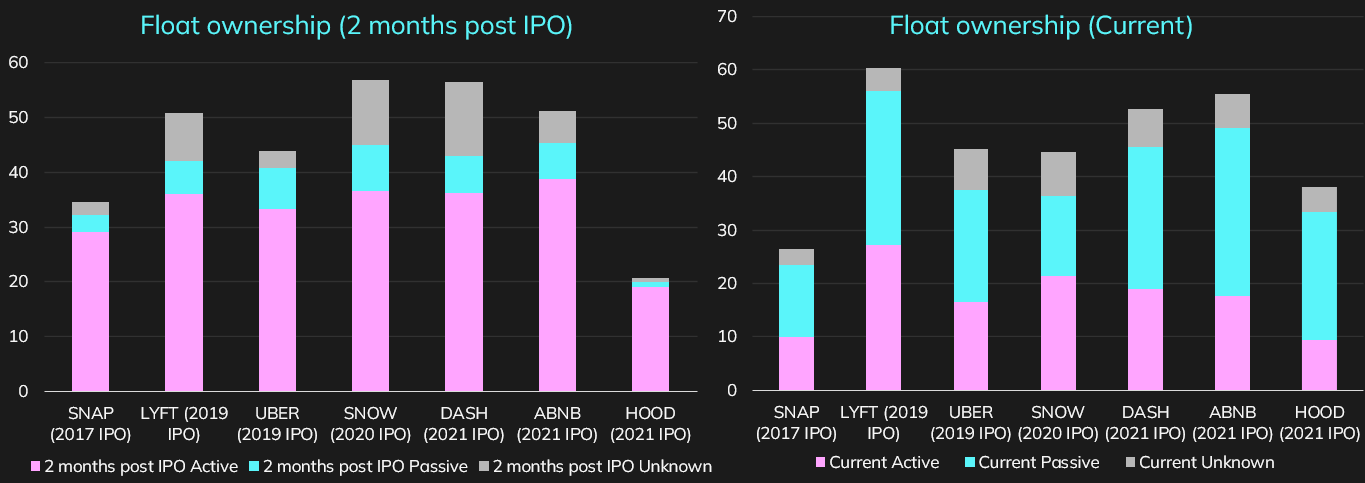

The chart below compares float ownership two months post-IPO against where those same names sit today. Passive stakes have built steadily since the IPO across every company, but during the IPO itself, active investors held the majority. That’s what drives early price discovery, and gives the wider market confidence in the valuation of shares.

Source: Bloomberg Note: Estimates based on measuring the portion of the shareholder base that is held by just US mutual funds and US ETFs, then splitting that subset into Active, Passive, and Unknown. This is a useful proxy of the traditional ownership structure of large US IPO’s.

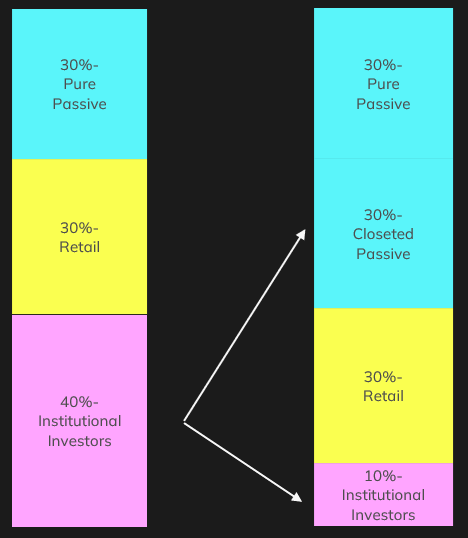

We contrast this with SpaceX’s expected ownership structure following the IPO. Intropic forecasts that c.30% of the free float will ultimately be held by direct index trackers, while c.25-30% has been allocated to retail investors. This leaves only c.41% of the float in the hands of active investors, a lower share than is typically observed following large-cap US IPOs, where ownership is generally dominated by active managers.

The implications become even more significant when accounting for the presence of “closet” indexers, active managers whose portfolios closely replicate benchmark indices. Academic research suggests that this segment may be comparable in size to traditional passive ownership. Under such a framework, the share of investors actively engaged in fundamental price discovery could fall to just c.10-40% of the shareholder base. In other words, a minority of owners may ultimately be responsible for determining the stock’s fundamental value.

SpaceX float ownership expectations (first 15 days)

Source: Intropic. Note: Forecast ownership of the tradable float following IPO and index inclusion. Active institutional ownership is expected to represent a minority of the shareholder base.

How do we see the IPO playing out?

Short term implications

Trading over the first week will be crucial

Retail investor participation, passive demand expectations, and reflexivity coming from options market makers could drive pricing upwards – irrespective of views on fundamentals. The low proportion of active participation could skew the IPO away from traditional views of valuation.

Trading outside of the first 3 weeks could be where “true” price discovery begins

Passive demand flows are expected to be prominent over the first 3 weeks of trading, which will materially effect price discovery. This could also lead to swings in price towards “true” value once the period of large structural demand flows passes. This could be further amplified by the price reversion post passive flow normalisation.

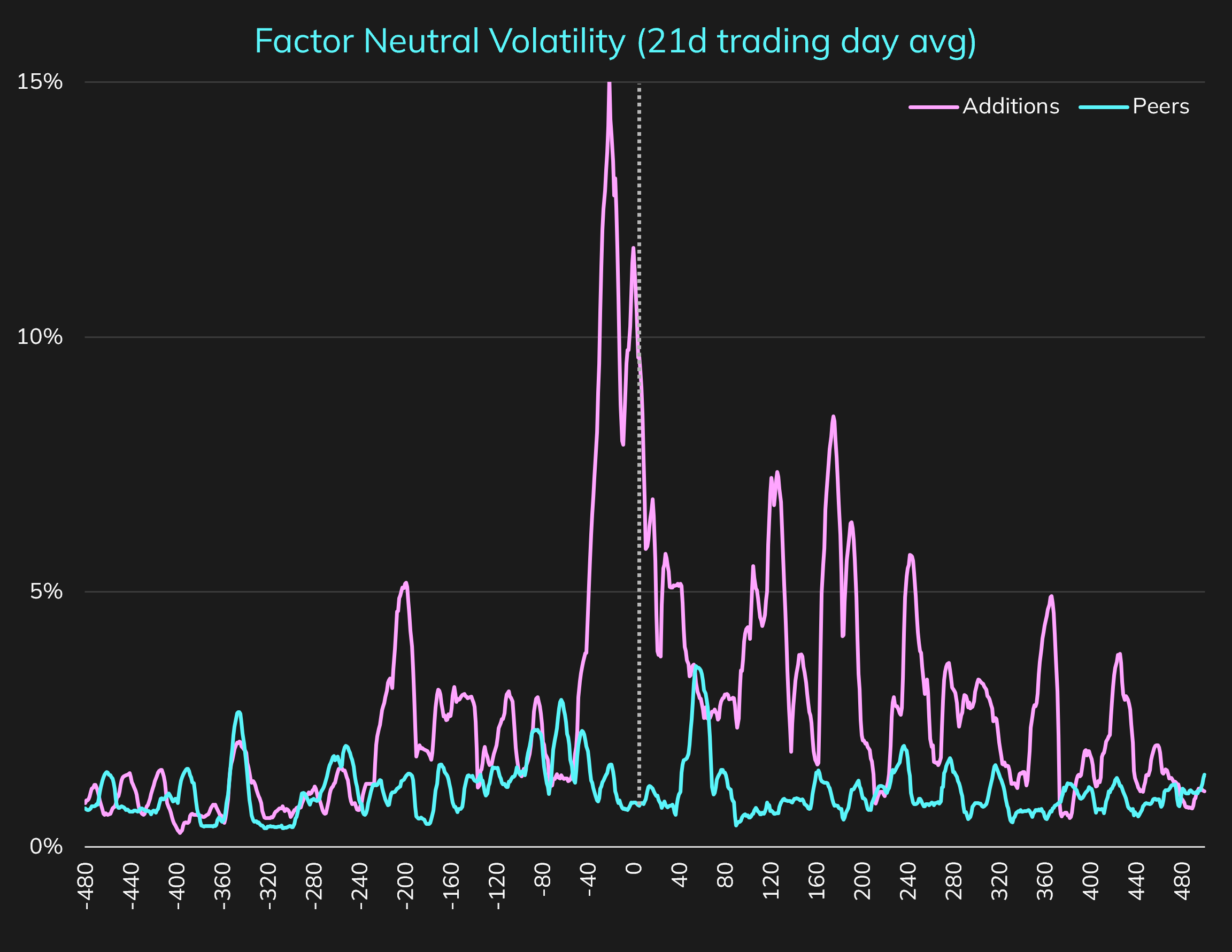

A very low proportion of investors will oversee pricing

This could lead to unprecedented levels of volatility over the course of its listing. A study we have run at Intropic looking at idiosyncratic volatility before and after a stock is added to the SP500 (whereby passive ownership increases and active ownership drops) – volatility increases, which we believe comes about because of the reduced “true” float. Extrapolating this to SpaceX’s fast entry across a variety of indices implies higher than usual levels of volatility.

Source: Axioma, Intropic.

Medium term implications

The stock will trade in closer correlation to its index-constituent counterparts

As a result of its fast entry into multiple indices, medium-to-long term stock co-movement to its index counterparts could be heightened – this is supported by empirical studies conducted, whereby stocks added to the S&P500 were judged to see higher co-movement with its peers in the long-term post addition. (Joseph DeCoste, Comovement and S&P 500 membership, Global Finance Journal, Volume 65, 2025.)

Lock-up expiries provide an opportunity for large blocks of share sell downs

However, these could be offset by structural demand from index re-weightings (which come about as a result of a material increase in the float, pushing index providers to upweight share ownership in its respective indices)

Source: Intropic

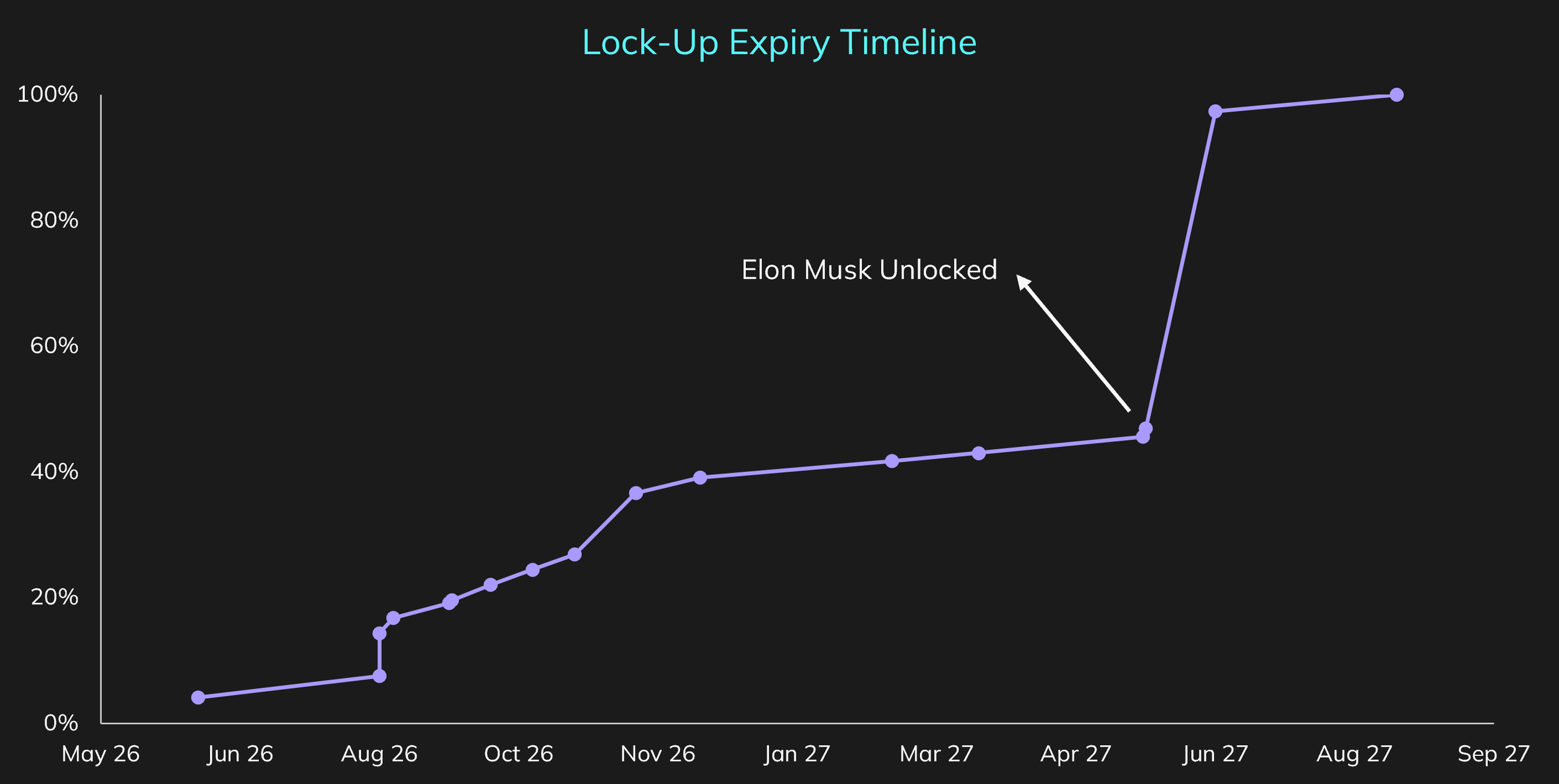

The lock-up schedule shapes how much stock reaches the market, and when. With a free-float of just 7.4%, the vast majority of the share base is locked up and released on a staggered timetable. Each expiry creates an opportunity for large block sell-downs, a supply overhang the market has to absorb. But the same jump in free-float can force index providers to upweight SpaceX at later reviews, which generates fresh passive buying that can offset the new supply. There are three main cohorts of locked-up holders, each on its own schedule:

Regular shareholders (4.7bn shares): All shares are free by Day 180, but 9 smaller partial unlocks across that window bring supply forward. A Q2 earnings release clause, alongside a stock-price early release trigger (130% of the IPO price) are the larger early release events, but the total by Day 180 is the same either way.

Significant investors (1.76bn shares): Larger pre-IPO backers, most likely Google, Valor and DFJ Growth, wait longest of the outside holders, on an extended lock-up. They too release in stages: six tranches between March 2027 and August 2027.

Elon Musk (up to 6.4bn shares): His whole stake stays locked for a full 366 days, unlocking in its entirety at once. About 1.3bn of it is tied to performance milestones, so although shares are contractually released, they remain milestone locked even after that date, leaving roughly 5.45bn actually sellable on the day.

Whilst Days 180 and 366 release the majority of shares, this is still a very aggressive unlock schedule compared with most. Most IPOs sit behind a single 180-day cliff, sometimes featuring earnings-based unlocks that shorten the period, or one or two small stock-price-conditional partial releases. In SpaceX, however, regular shareholders start selling within a couple of months of listing, so supply hits the market far sooner than in a typical deal, and is continuously drip-fed throughout the entirety of the lock-up.