SpaceX Game of Flows (Part III): What Happened in the First 7 Days of Trading

Our previous article detailed our expectations of how SpaceX would trade over the short-to-medium term. We presented the idea of reflexivity in the short term, with the convergence of a low-float, fixed batches of passive demand, and high retail ownership expected to drive prices. We also flagged volatility across the short and medium term given the low “true” active ownership. Prices did move sharply upwards over the first 3 days, surging 62% above the offer price at day 3, but more recently pared back to still a sizable premium to the initial offer.

We now look more deeply into what actually happened in the first seven days of trading, with day 5 driving c.£11bn of passive demand from index-linked funds.

The first seven days

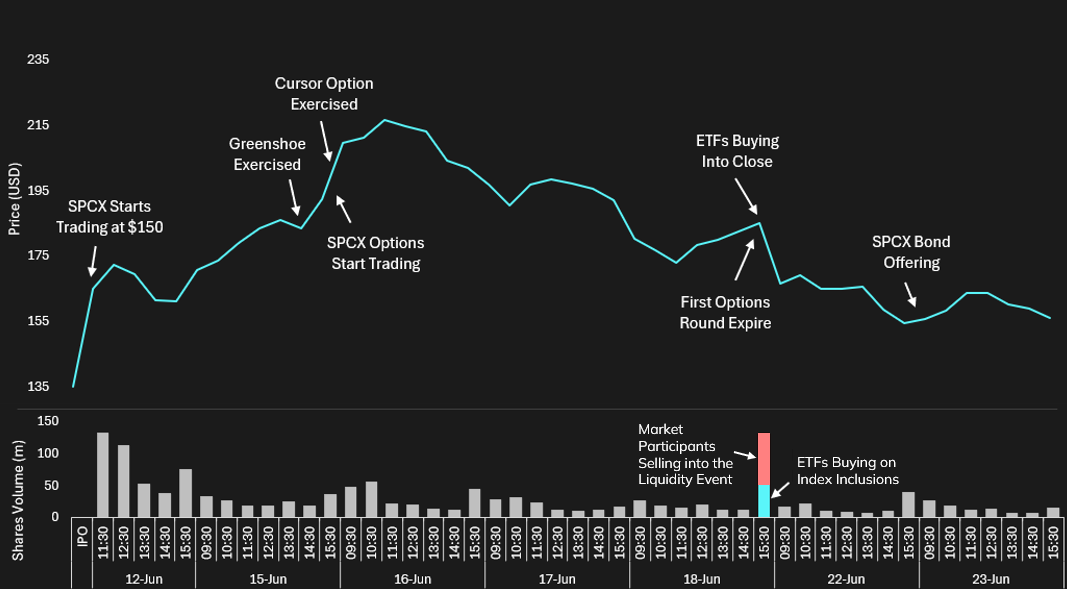

SpaceX listed on June 12, and the first day saw record retail buying, the biggest single day of US retail net buying ever, 50% above the previous record. With large institutions and a few active ETFs also building positions in the register, the stock closed c20% above its IPO price.

SpaceX Price Performance and Shares traded

Source: Intropic.

The June 12 close matters because it is the market cap the three index providers used to set their weights, which determined how many shares the passive funds bought on June 18. Some of that buying could have been brought forward to the 12th by index rebalance desks, but prepositioning into a new IPO is risky. We estimate more positioning to have come through between June 15 and 16.

These rebalance desks would have also been carrying the MRVL inclusion into the S&P 500, a much larger trade which settled the same day, tying up some of the risk they could have put on SpaceX. Whilst SpaceX’s trade might have not been fully prepositioned by the rebalance community, we did see negative price impact post the event. We believe that a large proportion of the Index demand was driven by other institutional participants looking to sell out of their postions. This selling activity was furthered by options expiries into June 18, with dealers unwinding the hedges they had built up over the week.

This is consistent with the reflexivity theme we set out in our previous note. As the inclusion approached, the expectation of passive demand drew in anticipatory buying, and that flow supported the price on the way up. After June 18, once the event passed and the non-discretionary bid was filled, that same support disappeared. The buying that drove SPCX higher into the event was the same buying that left it exposed once the event cleared, amplified by other market participants selling their stakes given the liquidity.

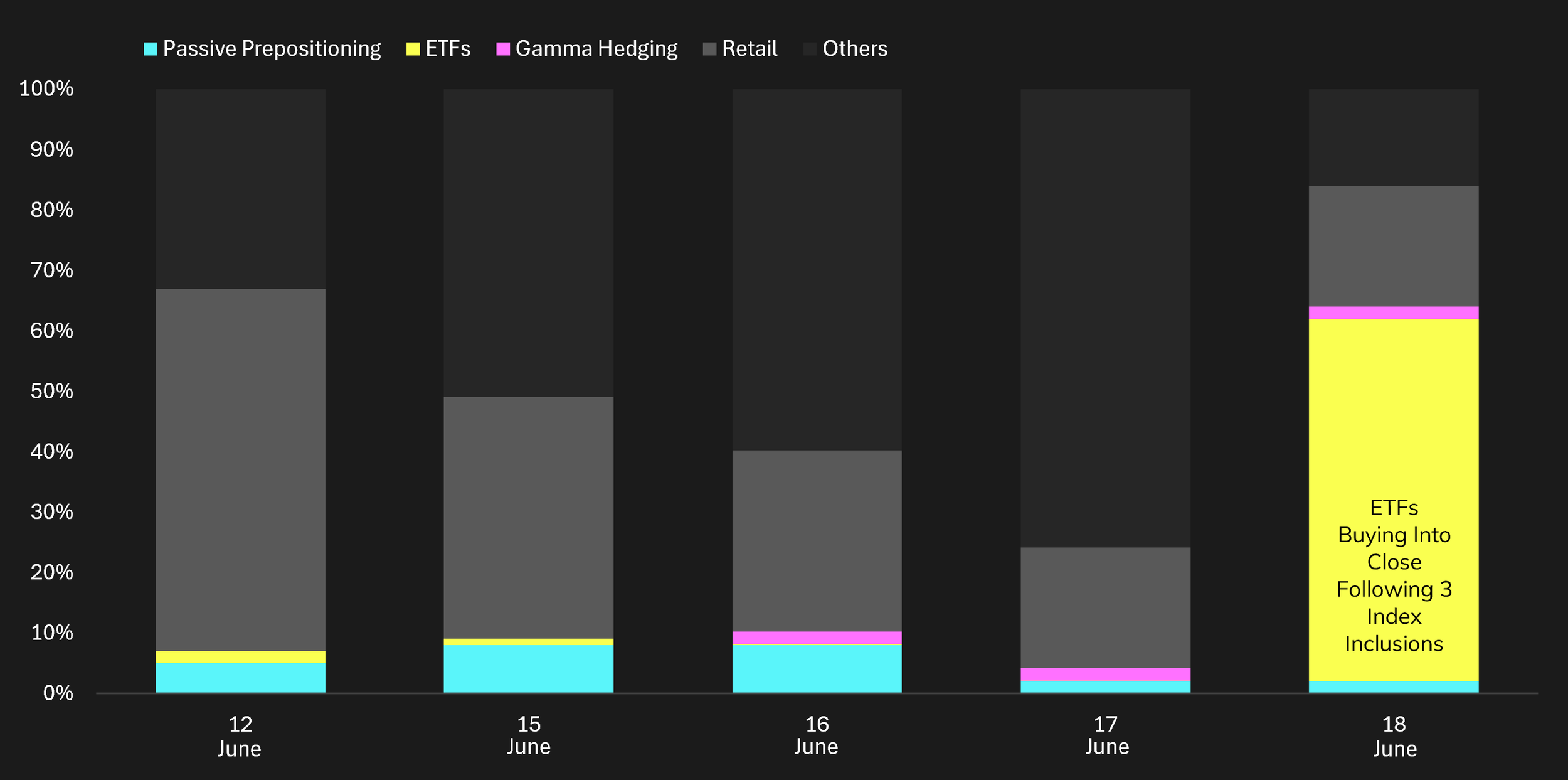

Estimated Share of Buying Volume Across the First 5 Days of Trading

Source: Intropic. Representation-only.

Will upcoming structural flows drive near-term upside?

With those competing inclusions and one-off events now behind, we expect to see some structural support from passive and retail flows.

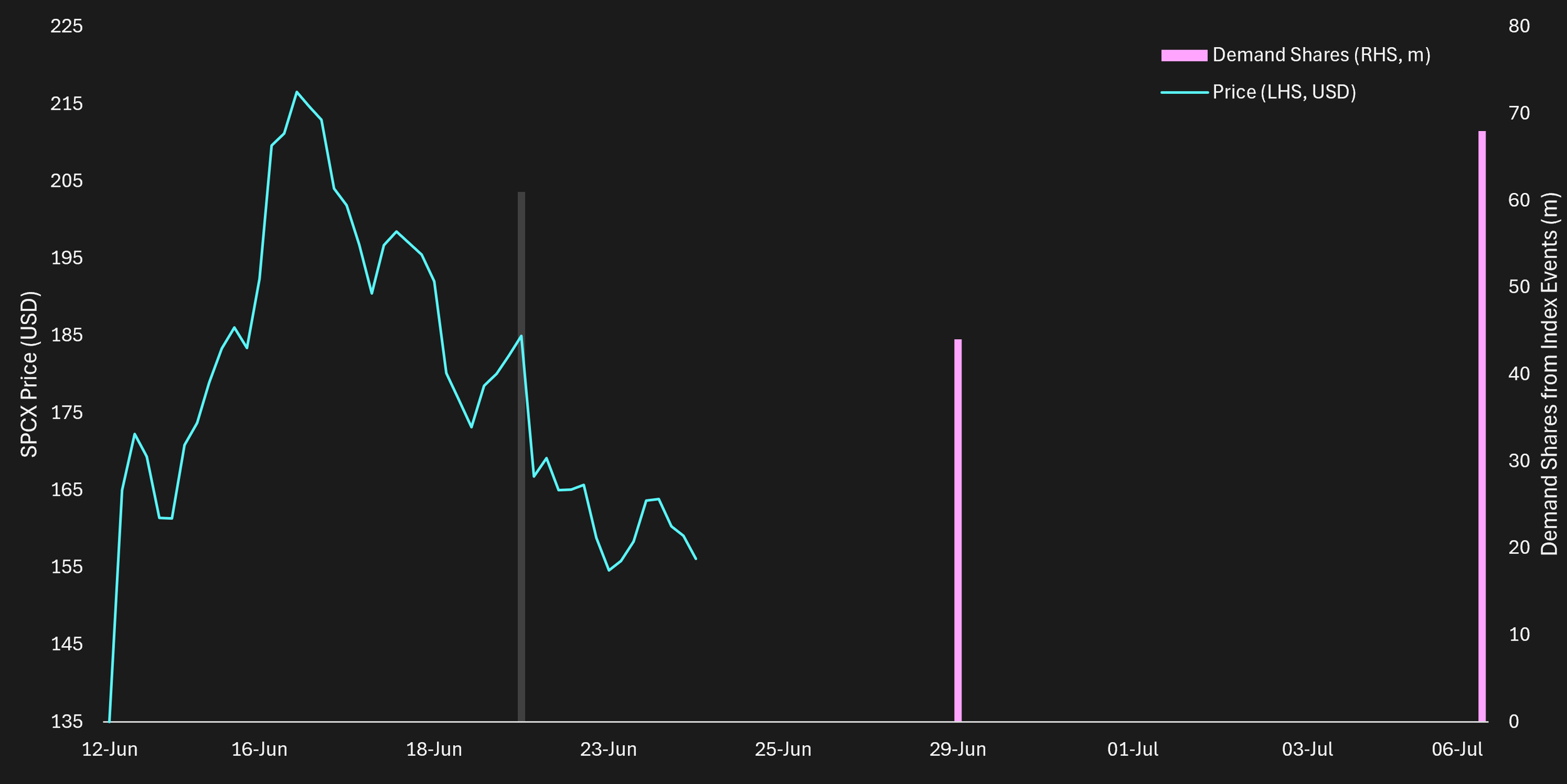

The initial index event on 18 Jun, leading to c.60m shares (c.$11bn) of index-linked demand, saw a downward move in share price by 7% the following session. Majority selling into the liquidity event looked to have driven the move, evidencing potential over-positioning led by non-traditional index players, with options expiry adding a further layer of downward pressure to share prices.

Daily volumes traded have now scaled back from IPO highs. Options expiries on 18 Jun were also a “one off” and should mean the pool of participants in the upcoming rebalances are more standard, with the longer run-up giving the opportunity for more normalised prepositioning.

This, coupled with expected seasonal retail inflows, adds potential structural support to shares. July is consistently one of the largest months for retail participation in the US, ranking second only to January on net capital deployed, as fresh allocations, retirement contributions, and a new half-year cycle bring retail back into the market.

This is well reflected in the seasonal performance of the largest indices. Since 1928, over 70% of 1H Julys have seen positive returns across both SPX and NDX. Upcoming index additions, could mean that the benefits of this are amplified.

Demand Shares from Upcoming Index Events

Source: Intropic.